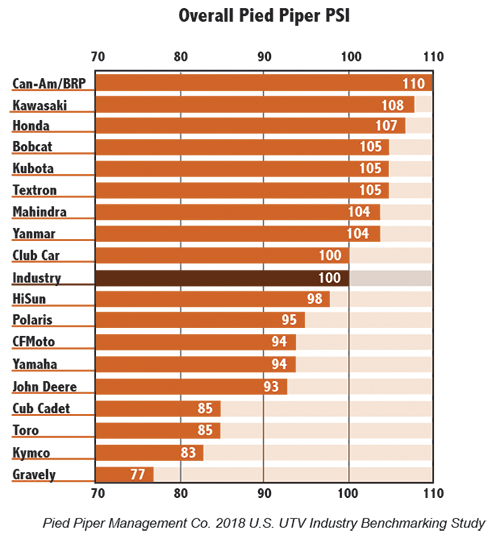

The first-of-its-kind prospect satisfaction index (PSI) for the U.S. UTV industry was recently released, with BRP’s Can-Am brand ranking No. 1 among 19 manufacturers. Kawasaki and Honda ranked second and third, while Bobcat, Kubota and Textron were tied for fourth. (See more rankings in the chart below.)

Pied Piper Management Co. conducted the survey, which measured the treatment of UTV shoppers. The company develops and runs measurement/improvement programs to maximize the performance of retail networks. The Pied Piper survey uncovered much more than rankings, however. Dealers can use the results as a road map for increasing satisfaction among their own customers.

“BRP is the ‘decathlete.’ BRP is the brand that tends to do well across the board. They may not be the top brand for every measurement, but they tend to have a process that they follow,” says Fran O’Hagan, president and CEO of Pied Piper. “We’re not a proponent of having the dealers sell the Pied Piper way or the BRP way. We want each dealer to take responsibility for their own sales process.”

Fran O’Hagan is president & CEO of Pied Piper Management Co. (Photo Courtesy Of: Pied Piper Management Co.)

O’Hagan says the process of selling and buying UTVs has distinct challenges related to the converging of the outdoor power equipment (OPE) and powersports markets. “It’s not always easy to be a UTV customer today. Because the UTV market is still young, strong dealerships with skilled salespeople are an important competitive advantage for UTV manufacturers,” he says.

O’Hagan shares more about the survey results in this conversation.

About the Study

Research Firm: Pied Piper Management Co. was founded in 2003 and is based in Monterey, Calif. The company develops and runs measurement/improvement programs to maximize the performance of retail networks.

Scope: The survey was conducted between July 2017 and April 2018 using 1,168 hired, anonymous “mystery shoppers” at dealerships located throughout the U.S.

Measurements: The survey looked at 60 different measurements were weighted to generate a score between 50 and 150. This was the first year for the survey, so the industry average was set at 100.

Rural Lifestyle Dealer: This is Pied Piper’s first experience researching this segment. What were your overall impressions of the OPE and powersports markets?

Fran O’Hagan: The UTV market overlaps two well-established industries that previously did not compete with each other for customers: powersports and OPE. Previously, the powersports industry focused mostly on leisure, while the OPE industry focused mostly on work. Today, for the UTV market, those boundaries are disappearing.

What I found fascinating is the approach that the OPE brands take in selling products is very, very different from the approach the powersports industry takes. I would argue that the OPE dealers think of their customers as people who they will have a long relationship with. They will sell tens of thousands of dollars of products to this person over many years, and service is just as important as selling the unit.

That is a very different approach from how a powersports dealer operates. Historically, the powersports dealers have thought of each sale as its own entity, almost to the point where the customer isn’t important.

RLD: Your approach is to use mystery shoppers as opposed to after-purchase surveys. Why do you choose that method?

O’Hagan: We found that after-purchase surveys were very misleading. Sales customers who purchased voted with their wallet. They must have liked the experience enough to make the purchase. As a result, sales customers give very high grades to their experience, whereas we know that it’s really only 1 or 2 customers out of 10 that buy on the spot. The other 8 or 9 walk back out again.

Also, when a customer walks into a dealership, they are focused on, “Do I buy this model or that model? Do I get this color or that color? Am I going to finance this or am I going to buy? Is this dealership going to take my trade? How long is this going to take?” The customer is not at all focused on things, such as how effectively the salesperson is building rapport or fact-finding.

RLD: What kind of information did your mystery shoppers gather and how did the data factor into the ratings?

O’Hagan: The survey ties sales behaviors to sales success. We’re able to say that dealers who outperform other dealers tend to exhibit certain behaviors. If we do this over and over again with hundreds of different dealerships, all of a sudden the factual measurements that are important bubble up to the top. That leaves us with some quantity of behaviors to measure and for UTVs, it’s a little over 60.

We use mystery shoppers to generate PSI measurements, but we’re not at all interested in the mystery shopper’s opinion. To us, a mystery shopper is just an actor going through the motions, who is measuring whether certain behavior happened or not.

RLD: Can you comment on the behaviors that helped BRP (Can-Am), Kawasaki and Honda top the satisfaction ratings?

O’Hagan: It’s interesting to look at something like test drives. For example, 38% of the time Honda salespeople offered a test drive on the spot. BRP was only 22% and Kawasaki was only 21%. With 60 different measurements, BRP will be at the top some of the time and there are others where Kawasaki will be at the top. It’s only the weighted average across all 60 that generates those final scores.

Here’s another example: the “poor man’s test drive,” encouraging the customer to sit inside the vehicle. It seems like that would be basic. For BRP, that happens two-thirds of the time. For Cub Cadet, that happens one-third of the time.

RLD Podcasts Continue the Discussion

Hear more from Steve Shankin, president of ViaLink and Seizmik, about the UTV market and how dealers can earn more sales. Go to www.RuralLifestyleDealer.com/UTVMissedOpportunities. Watch for an upcoming podcast with Fran O’Hagan, president and CEO of Pied Piper Management Co., about the 2018 Pied Piper Prospect Satisfaction Index U.S. UTV Industry Study.

Rural Lifestyle Dealer’s podcast series is brought to you by Yanmar.

![]()

RLD: Why do you think it is difficult to be a UTV customer today?

O’Hagan: Some products are very easy to research. If you want to buy a car, there are third-party websites that analyze cars exhaustively. If you figure out you want a compact sport utility that costs between $20,000 and $30,000, third-party websites will pop up and show you four to consider and why.

RLD: You had mentioned earlier that there is no one way to sell UTVs. Can you explain more?That is not the case with the UTV market. There are some brands that sell UTVs very well and for others, UTVs are an afterthought. Their primary products are something else, so it’s difficult to find product information. What’s more, it can be difficult or even misleading to figure out which of their dealerships sell UTVs. You go to their website to find the closest UTV dealer and it might not show that info. And even if it does, if you call that dealer, you’re likely to hear, “Oh, we don’t carry UTVs.”

O’Hagan: Our advice to the manufacturer is that the retailers need to have a very simple sales process in writing. I’m talking maybe 3-5 steps, something that’s easy for salespeople to remember. Here is an example.

1. Build rapport and sell yourself. Make a positive first impression with the customer. Ideally, strike up a conversation and avoid asking a question such as, “How can I help you?” to which the customer can answer, “I’m just looking.”

2. Ask about the customer; sell the dealership. Learn why the customer is in your dealership. Confirm that the customer has come to the right place.

3. Involve the customer; sell the product. Do all you can to involve the customer rather than just talking at them. Have them sit in a vehicle, take it for a test drive, and point out specific relevant features and benefits.

4. Move from learning to buying; ask for the sale. Suggest sitting down at a desk and going through the numbers. Pave the way for the customer to say “yes.”

5. Get contact information and follow up. About 8 in 10 customers will not buy on the spot, but they will buy later and will influence others who will buy.

To give you an example of the differences in terms of asking for the sale, Bobcat salespeople encourage going through the numbers or writing up a deal 59% of the time, while Toro dealers do that 27% of the time. (See the charts to see how the brands scored on various sales behaviors.)

“It’s not always easy to be a UTV customer today…”

–Fran O’Hagan of Pied Piper

RLD: What about dealerships that sell multiple brands. What did your survey uncover?

O’Hagan: One thing we find fascinating is what happens when a customer visits a multi-line dealership, asking about a specific brand and a salesperson says, “Oh, that’s interesting, but have you considered this brand instead?” For every brand, we measure how often salespeople pitch a different brand instead. For the UTV market, the math is all over the place.

For a brand like Textron or CFMOTO or Yamaha, more than 25% of the time when customers come in saying, “I’m interested in this Textron UTV,” the salespeople try to sell them another brand instead. We don’t allow our mystery shoppers to go down that route, but we make a note of it. The opposite happens for Bobcat, John Deere and Mahindra, when salespeople do that less than 10% of the time. That’s partly because many Bobcat or John Deere locations don’t have other brands. Maybe they have used ones, but it’s really more of an issue at the multi-line dealerships.

RLD: Can dealers use your surveying tools?

O’Hagan: They can. Our business is helping brands and manufacturers, but almost 15 years ago, dealers began contacting us saying they had been introduced to us through brand A, but they sell brands B, C and D and wanted to measure how they sell all their brands. We created an application where they can order PSI mystery shoppers online.

Commentary:

Why the Brands Ranked as They Did

Steve Shankin is president of ViaLink and Seizmik. ViaLink consults with manufacturers on UTV development and Seizmik is the leader in aftermarket UTV accessories. Here is Shankin’s take on the 2018 Pied Piper Prospect Satisfaction Index U.S. UTV Industry Study.

Steve Shankin is president of ViaLink and Seizmik. ViaLink consults with manufacturers on UTV development and Seizmik is the leader in aftermarket UTV accessories. Here is Shankin’s take on the 2018 Pied Piper Prospect Satisfaction Index U.S. UTV Industry Study.

Polaris is ranked comparatively low, but has the highest market share by far. Can-Am is ranked highest, but has relatively low market share. They were also the fastest growing of the top 10 brands by far. I conclude from this that the Polaris dealers aren’t trying all that hard because they don’t really have to. Polaris spends $16 million per year in advertising their off-road vehicles and they have a staggering lead in market share. Customers probably show up at Polaris dealers ready to buy.

Meanwhile, Can-Am has launched some very exciting new vehicles in the last couple of years and are seriously challenging Polaris, but they’re still in a super-distant fourth place in market share. They’re trying harder and are more engaged because they have to be. I could say the same thing about Honda and Kawasaki.

It doesn’t surprise me at all that Gravely/Ariens is dead last with a 77. Their vehicle is simply a rebranded Polaris Ranger with a few changes. Their dealers have probably already found out that there isn’t much that they can do to win customers, so they’ve stopped trying. Polaris sold more than 170 times more vehicles than Gravely. I’m not talking about percent, I’m saying when you take the number of units Gravely sold and multiply it by 170, you get reasonably close to the unit number for Polaris.

The report says, “Previously, the powersports industry focused mostly on leisure, while the Outdoor Power Equipment industry focused mostly on work. Today, for the UTV market, those boundaries are disappearing.”

I don’t find this statement to be accurate at all. Certainly, it’s true that the OPE market does not focus on leisure. In fact, they don’t really participate in that segment in any significant way. The “leisure market” is only about 30% of the total UTV market and in the powersports channel, there are definitely more work/crossover vehicles (like the Polaris Ranger) sold than anything else.

In reality, the powersports market overlaps completely with the OPE market and it’s always been that way. There is no doubt that both channels compete with each other in all segments other than “leisure.” (Photo Courtesy Of: Steve Shankin)

Post a comment

Report Abusive Comment