Financial Results

-

Second quarter revenues totaled $7 billion, down 10% compared to Q2 2014 on a constant currency basis (down 22% on a reported basis). Net sales of Industrial Activities were $6.6 billion, down 10% compared to Q2 2014 on a constant currency basis (down 23% on a reported basis).

-

Operating profit of Industrial Activities for the quarter was $401 million ($678 million in Q2 2014), with operating margin at 6.0% (7.9% in Q2 2014).

-

Costs for research and development and selling, general and administrative expenses were $851 million in Q2 2015, down $199 million or 19% compared to Q2 2014.

-

Net income was $122 million, or $0.09 per share. Net income before restructuring and other exceptional items was $141 million, or $0.11 per share, down $241 million compared to Q2 2014.

-

Net industrial debt was $3 billion at June 30, 2015 ($3.1 billion at March 31, 2015). Available liquidity totaled $7.8 billion ($7.2 billion at March 31, 2015).

-

Full year guidance updated as follows: net sales of Industrial Activities in the range of $26-27 billion, with operating margin of Industrial Activities between 5.6% and 6.0% and net industrial debt at the end of 2015 between $2 billion and $2.2 billion.

2015 Second Quarter Results

London — CNH Industrial N.V. today announced consolidated revenues of $6,958 million for the second quarter of 2015, down 10% compared to Q2 2014 on a constant currency basis (21.9% on a reported basis). Net sales of Industrial Activities were $6,634 million in Q2 2015, down 10% compared to Q2 2014 on a constant currency basis (22.5% on a reported basis). Excluding the negative impact of currency translation, net sales increased for Commercial Vehicles (up 11.9%) confirming a positive trend in EMEA for trucks and buses. This increase was more than offset by the forecasted protracted decline in Agricultural Equipment, driven by lower industry volumes in the row-crop sector and dealer inventory de-stocking actions, primarily in NAFTA, slightly offset by favorable net pricing in all regions. Furthermore, net sales decreased in Construction Equipment, due to negative industry volumes primarily in LATAM, and in Powertrain, due to lower sales to captive customers.

Agricultural Equipment

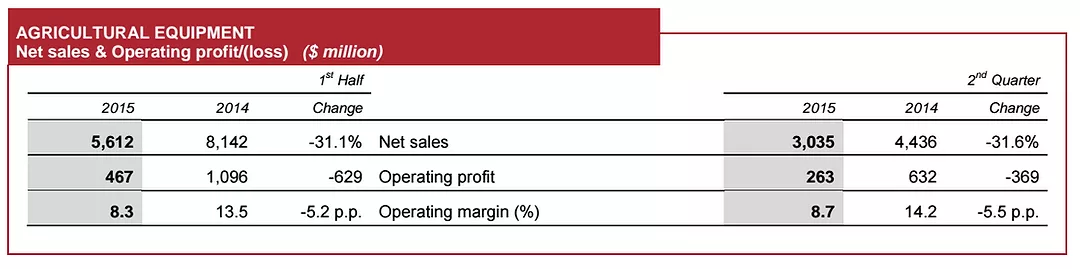

Agricultural Equipment’s net sales were $3,035 million for the quarter, down 23.7% compared to Q2 2014 on a constant currency basis (down 31.6% on a reported basis). The decrease was driven by the anticipated decline in industry volumes in the row-crop sector and dealer inventory de-stocking actions, primarily in NAFTA, slightly offset by favorable net pricing in all regions. The geographic distribution of net sales for the period was 38% NAFTA, 39% EMEA, 10% LATAM and 13% APAC.

In the company’s key product segments in NAFTA, the over 140 horsepower (“hp”) tractor segment as well as the combine segment were down 31%. The under 40 hp tractor segment in the region was up 5%, and the 40-140 hp tractor segment was up 2%. EMEA markets were down 7% for tractors and 9% for combines. In LATAM, tractor and combine markets decreased 26% and 19%, respectively. APAC markets decreased 3% for tractors and 17% for combines. Worldwide agricultural equipment industry unit sales were down 4% for tractors and down 17% for combines.

The company’s market share performance in Agricultural Equipment was mixed in the second quarter. Tractor market share improved in all markets, most significantly in the higher horsepower tractor segment in NAFTA, while market share declined in the under 40 hp tractor segment in NAFTA. For combines, market share decreased in all regions, after a strong performance in Q1 2015. For the six-month period, the company’s market share was generally up in both tractors and combines.

In Q2 2015, Agricultural Equipment’s worldwide unit production was 14% below retail sales in the continued effort to reduce channel inventory and align production with current demand. The finished goods inventory for the company and its dealers declined approximately a combined $700 million since Q2 2014, and current production levels are expected to further drive down total inventory levels in the second half of 2015.

Agricultural Equipment’s operating profit was $263 million for the quarter ($632 million in Q2 2014), with an operating margin of 8.7% (14.2 % in Q2 2014). The year-over-year change was driven by lower sales volume and less favorable product mix in the row-crop sector, primarily in NAFTA, and by negative foreign exchange impacts, primarily as a result of the sharp weakening of the euro and the Brazilian real. Those effects were slightly offset by positive net pricing and cost control actions, including purchasing efficiencies and structural cost reductions.

2015 Guidance

As a result of continued demand weakness in the agricultural row crop sector and in order to foster additional clearing of finished goods inventory, primarily in the North American and LATAM markets, the Company will adjust production accordingly in the second half of 2015.

Full year guidance is therefore updated as follows to reflect the negative impact on operating margin and the positive impact on working capital due to these production adjustments:

- Net sales of Industrial Activities in the range of $26-27 billion, with an operating margin of Industrial Activities between 5.6% and 6.0%;

- Net industrial debt at the end of 2015 between $2.0 billion and $2.2 billion.