Times are tough for producers, and dealers need a silver lining. Between the chaos caused by late planting, followed by the cloud of uncertainty created by the trade disputes with China, equipment dealers’ sentiment came in lower in this year’s Ag Equipment Intelligence 2020 Business Outlook & Trends Farm Equipment Forecast. Nearly 3% fewer dealers (41.7%) forecast increased new farm equipment sales in the coming year than did in last year’s Business Outlook & Trends report (44.6%).

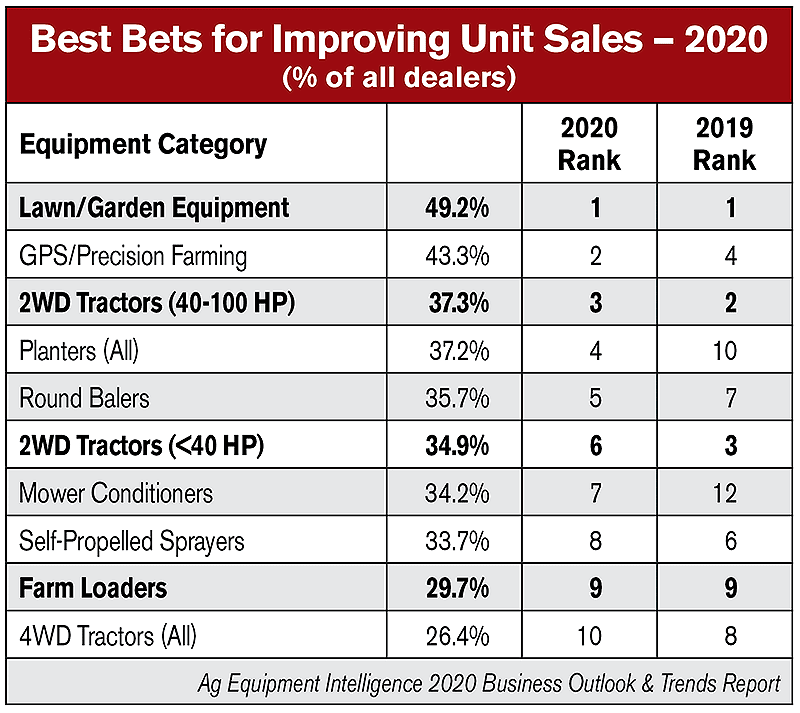

Despite this modest fall in overall optimism, lawn and garden equipment peaked again as the top equipment category that North American dealers expect to increase sales revenue in 2020. When looking at the full list, lawn and garden equipment came in first at 49.2%, followed by GPS/precision farming at 43.3% and utility tractors (40-100 horsepower) at 37.3%. Lawn and garden equipment also had the highest percentage of dealers betting on it for an increase in sales revenue by 8% or more, at 10.8%.

The second most popular equipment category forecast for improved unit sales of 8% or more was compact tractors (under 40 horsepower) at 9.9%. Farm loaders also appeared as the 10th most popular selection for dealers looking ahead to next year, at 29.7%.

Maintaining Strong Trend

This isn’t the first time small equipment categories have made it to the top of dealers’ most favored items for increasing sales. In last year’s 2019 Business Outlook & Trends report, of the top 5 picks for dealers’ “Best Bets,” 3 were small ag equipment, including lawn and garden equipment at 53.6%, utility tractors at 45% and compact tractors at 44.1%. Farm loaders also came in 9th place at 30.7%.

Lawn and garden equipment topping the charts these last 2 years is the tip of the iceberg. This year’s “Best Bets” continues a trend that began in the 2016 Business Outlook & Trends report, when lawn and garden equipment first crept to the top of the list for dealers’ “Best Bets” at 39.6% and it has been at the top ever since.

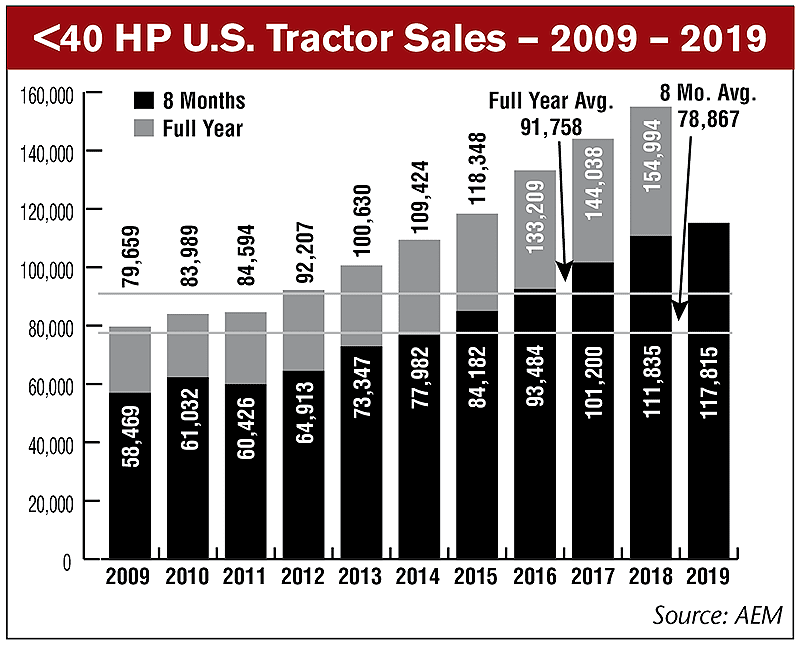

Compact tractors came in 6th place for the 2020 report at 34.9%, down 3 places and 9.2% from its placement in the 2019 report. In spite of this, the future for compact tractors looks bright, as unit sales for this class of equipment have been increasing gradually since 2009.

As reported by the Assn. of Equipment Manufacturers (AEM), U.S. sales of under 40 horsepower tractors have been on a steady incline at both the 8-month and full-year level for the past 11 years. Sales for this year’s 8-month period have reached 117,815, beating out the 8-month measurement of 2018’s sales (111,835) by 5.1%. Even Canadian dealers, who have experienced declines in most equipment sales categories, saw marginal improvements in compact tractors sales over the last several years at the 8-month mark, reaching 9,302 in 2017, 9,700 in 2018 and 9,869 in 2019.

Small equipment dealers’ customer demographics are also shifting, with the two measured in the report being hobby farmers and turf, lawn and landscapers. In the 2020 Business Outlook and Trends report, the total percentage of North American dealer revenue that comes from hobby farmers was reported at 17.4%, a 0.3% increase over the 17.1% reported last year. However, the percentage of revenue coming from turf, lawn and landscapers decreased overall, from 9.4% last year to a little over 8% this year. U.S. dealers saw an increase in the percentage of their revenue coming from hobby farmers, from 17.7% in the 2019 report to 18.7% in this year’s 2020 report. Turf, lawn and landscaper revenue percentages decreased even in the U.S. market, however, from 9.1% last year to just over 8% this year.

All in all, dealers operating on the small equipment side can afford to be a little more optimistic than large ag equipment dealers and possibly even a little hopeful for next year’s growing season.