Studies show that if you help a customer arrange financing, they are three times more likely to go to your dealership first the next time they’re looking to purchase equipment. They are also 2½ times more likely to buy from you again. If you helped them finance a purchase, there is a 75% chance that they will finance their next purchase with you as well, according to statistics from lender DLL.

Despite the advantages, dealers share these obstacles: Applications are too strict, too bulky or require written signatures; lenders aren’t open when rural lifestylers are shopping; and the inability to submit electronically to different lenders at once, an established practice in the auto industry.

Lending experts share their thoughts on those challenges as well as what dealers need to know about what’s changing.

Investing in Technology

Mac Braun, senior vice president of agriculture and golf and turf markets at Wells Fargo Equipment Finance, says that FDIC has ranked Wells Fargo as the largest farm lender for the last 20 years, and about 20% of its business is for the rural equipment market. He shares what Wells Fargo is doing to support rural equipment dealers. “It’s one word — speed. We’re improving our systems to become faster and move customers from shoppers to owners. We’re investing in technology processes and procedures to become more automated,” he says.

Mac Braun is senior vice president of agriculture and golf and turf markets at Wells Fargo Equipment Finance.

Current submittal and approval process can be done through an online portal or through a sales representative. However, there is no automatic decision. In terms of dealer concerns about process, he says, “We hear. We agree. We’re working on it.” He expects the company will implement new technology in the next several months that will help address the 24/7 demands for loan applications.

Braun says it can be difficult to compete with the 0% interest rates that manufacturers offer. However, they can compete on standard rate terms, and they do have programs in place with shortline manufacturers.

Braun says relationships and education are key to making financing work for the dealer and the customer. “I think education is key when it comes to financing, and I believe in learning by doing. I encourage getting in there and forcing yourself to use financing in a transaction to help build your confidence with a customer,” he says.

How can dealers not lose a sale? “Ask questions of the lender when you see a decline. Ask questions about whether an additional down payment, a loan guarantor or a shorter structure could help,” Braun says.

Providing Options

Cleo Franklin is the vice president of marketing and strategic planning and chief marketing officer for Mahindra North America.

Cleo Franklin, Mahindra North America’s vice president of marketing and strategic planning and chief marketing officer, says Mahindra tries to keep in mind what customers are accustomed to regarding financing outside of the equipment market and tries to think differently.

“We introduced 0% for 84 months in April of 2013, an ‘industry first’ for tractor financing. Last year, we extended 0% for 84 months to our utility vehicles and provide 0 down and 0 interest as well for Mahindra products,” Franklin says. “Longer term financing with 0% down and 0% interest may have been foreign years ago in our industry, however this type of financing has been well known and commonplace to the customers we support.

“Our customers who are rural lifestylers like flexibility, 0% down, payment waivers and longer terms — consistent with what they’re getting when they go to Best Buy, Home Depot or the car dealership for their vehicle,” Franklin says.

Dealer Takeaways

Develop an arsenal of financing options so you can serve customers with all levels of credit history.

Don’t give up if a customer is initially denied credit. Work with the financing company on such alternatives as larger payments, shorter terms and co-signers.

Keep updated on what your financing partners might be offering. For instance, make sure your dealership is able to support new mobile application processes.

Packaging maintenance into the financing can be another advantage in winning sales. Mahindra recently introduced its 7-7-7 program, which includes a 7-year warranty, 7 years of 0% interest and a 7-year service plan. “When you can bundle and finance the total product and support the package, you simplify the process for the customer and make it very easy for them to buy,” Franklin says. “In our industry, when a customer comes into one of our dealerships, it’s important to provide them with a ‘one-stop shop’ destination to handle all their needs to help transition a prospect into a buyer.”

Closing the deal requires a variety of options: manufacturer financing, secondary lenders, rental and leasing options.

“You always have the dynamic when a customer comes in with a challenging credit background. What has gotten better is the multiple options that exist today. At the end of the day, in our business, reality sets in and there will be times when there are some deals that just can’t be made. The most important thing is to try think differently and bring forward different solutions and options, and let the customer decide what is best for them,” Franklin says.

Building Relationships

Jack Snow is the president of Sheffield Financial.

Jack Snow and his wife Bonnie started Sheffield Financial in 1992. Since that date, the Clemmons, N.C.-based company has financed over $16 billion in consumer and commercial installment retail loans for outdoor power equipment, powersport vehicles and one-axle trailers. Branch Banking & Trust acquired Sheffield Financial in 1997.

“In 2002, we were financing one out of every three mid-sized lawn mowers sold, and we’re still financing one out of every three. We do $1 billion of retail financing in just lawn mowers each year. We’re very competitive, even with captive finance companies,” Snow says. “In just 15 seconds, a lot of our competitors can make a decision on a loan using computer software. We have human beings looking for recommendations from our software. We look more for stability than we do credit score.”

He says part of what helps them compete is their easy application process plus the ability to talk with one of the 50 underwriters on staff if an application is denied — something he encourages dealers to do more of.

“After a few times of ‘holding hands,’ dealers get to know the underwriters and build personal relationships. This is very, very important because there are going to be times you are going to need that for your customers,” Snow says. “Dealers are becoming savvier about financing, the bigger dealerships and the smaller ones. In a day’s time, a dealer can turn financing into a profit center. Most OEMs don’t mind adding in things to the financing like an extended warranty or a grass catcher.”

“In a day’s time, a dealer can turn financing into a profit center…”

— Jack Snow, Sheffield Financial

Snow is planning for growth, hoping to double the size of Sheffield in the next four years. “We’re going to ‘make a splash’ in home building products, like generators and heat pumps. We’re also looking into other opportunities in the powersports business such as pontoon boats,” he says. Another market he’s considering pursuing: quilting machines, which can retail for as much as $30,000.

In the midst of growth, Snow is also watching regulatory changes. “I’ve seen a lot of changes in the last 7 or 8 years. We’re seeing regulators scrutinizing the larger banks, but also the smaller banks and that may be trending all the way down to the dealer network. Regulators want to know that we’re working with legitimate dealers; that they’re not laundering money. And, then, sometimes, they ask the question, ‘How do you know that the customer the dealer is doing business with is not laundering money?’ If it continues on this path, it could get down in the weeds, but that would be many years away. And, if the administration or atmosphere changes in Washington, we may never see it.”

Closing the Sale

Gustavo Lichtenberger is DLL’s vice president of strategic marketing, food and agriculture.

DLL offers retail financing for the full spectrum of credit ranges and has relationships established with 15 rural equipment manufacturers. “What makes us different is our commitment to this market. All dealers and all customers in the rural equipment market are important, no matter the size of the transaction,” says Javier Pelaez, DLL’s director of program management, food and agriculture.

For those with challenging credit, DLL underwriters offer at least two options to make a deal such as increasing the down payment or adding a co-signer. Some dealers provide support if they believe a customer is worth the risk.

DLL offers online contracts; automatic decisions; Saturday hours and extended hours during the week. “Speed is a critical factor. Dealers cannot afford to have customers leave the facility to shop around,” says Gustavo Lichtenberger, DLL’s vice president of strategic marketing, food and agriculture. “Two or three years ago, online application submissions were around 30%, and now it’s averaging 80-90%. We’re essentially getting to the point of our entire business coming to us online.”

Lichtenberger says they recently streamlined the application process, and they are now investing in mobile technology. This means the company’s interface will be adapted so that applications can be easily submitted through a mobile device or tablet in addition to the traditional computer method. DLL is hoping to launch the mobile technology by the end of the year.

Understanding the Benefits of Leasing

Leasing in the equipment industry has traditionally been concentrated in the large construction or ag equipment segments to help customers afford big machines with high price tags. However, rural equipment dealers may want to take a look at the arrangement as a new way to sell to light construction companies, landscapers, small acreage farmers and even large property owners.

“What’s changed now in the rural equipment market is the price of the equipment. Entrepreneurs who may need to purchase equipment for their landscaping businesses, for example, face spending $40,000-$50,000. They’re asking, ‘How can I afford this?’ Dealers are looking for ways to offset that concern. It all comes down to affordability and cashflow,” says James Falk, director of knowledge management for DLL.

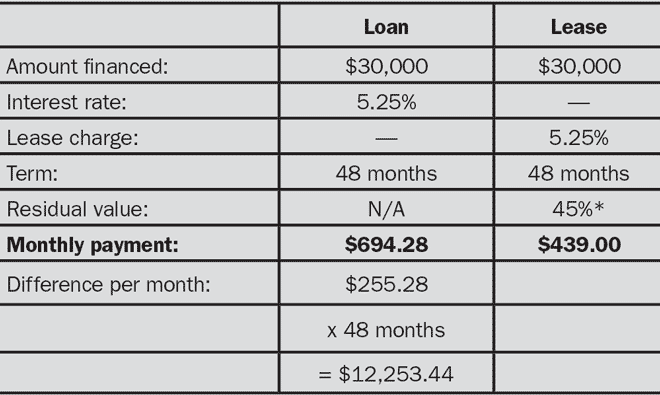

“In order to make monthly payments affordable for purchased equipment, some of the financing terms may stretch to 84 months. The problem with that arrangement is some customers don’t necessarily want to keep a machine around that long because of the potential repairs they’ll face. Also, purchase arrangements may require a 10-20% down payment, while leases generally require only two lease payments upfront. These are just some of the potential benefits of leasing,” Falk says. (Refer to the chart “Comparison of Loans vs. Leases”)

Falk also says leasing addresses the issue of the rising cost of rural equipment, which is making it even more challenging for customers to afford new equipment or stay current with equipment.

“Many of your competitors are not offering leasing options, so it’s a good way to differentiate your dealership. Offering additional financing options means you have a greater chance of meeting customers’ needs, and they are less likely to continue shopping at other dealerships.”

“Also, by showing them the lower monthly payment, regardless of whether they choose a leasing arrangement, you provide the perception that the equipment your dealership sells is more affordable,” Falk says.

DLL is also offering leasing options for rural equipment. (See the sidebar “Understanding the Benefits of Leasing” on page 30.) Affordability and cashflow are key advantages, and Pelaez offers another: “Leases help offset the trend toward longer and longer loans, which keeps customers out of the market for extended periods of time. The fact of the matter is that leasing, in most cases, guarantees that the customer will need a new piece of equipment in 4 or 5 years when their lease expires,” he says.

Comparison of Loans vs. Leases

That’s $ 3,063.36 per year.

* The residual value is the amount the lender believes the equipment will be worth at lease-end. At that time, the customer might have the option to extend the lease, buy the equipment, trade the equipment or return the equipment to the dealership. Rates and residual values can vary based on several factors including the type of equipment, terms of the loan or lease, hours of use and, sometimes, even the customer’s credit worthiness.

Lichtenberger comments on the advantage that auto dealers have of submitting to several lenders and why a third party vendor hasn’t yet developed the functionality for rural equipment. “The main reason is scale. Whatever happens in the auto sector is orders of magnitude larger,” he says.

Lichtenberger offers these strategies for dealers: “Don’t assume buyers want the lowest payment. Some people are more interested in reliability. Additionally, they might want to maintain the manufacturer’s warranty. An extended contract term might prevent a new sale or put your customer in a negative equity position for an extended period of time.”

He says dealers should ask themselves the following questions:

- How many sales would you like to make to a customer within 84 months? One, two?

- What would happen to your bottom line if you could make more than two?

- Are you taking trades? Do you make money on them?

Dealer View from Georgia

Bruce Purcell owns Quik-Kut Power Equipment of Claxton, Ga. Purcell says that about half of his customers take advantage of the 0% financing offered through Sheffield.

Bruce Purcell owns Quik-Kut Power Equipment of Claxton, Ga., and carries Echo, Grasshopper, Shindaiwa, Scag and Toro. Purcell says that about half of his customers take advantage of the 0% financing through Sheffield. Around 30% or so are government contracts and the remainder pay cash. He’s been working with Sheffield since the early 1990s and says the relationship and service from Sheffield has helped his business grow. “I cannot say enough good things about what Sheffield has done for my business,” Purcell says.

Purcell handles most of the sales, but says anybody at his dealership can help with the credit application. Financing discussions come toward the end of the sales process for him.

“I have to talk with the customer to get them ready to make a purchase. I talk about the durable and comfortable mowers and get them sold on the mower itself. Then, I tell them, ‘Oh, by the way, there’s 0% financing for 48 months with nothing down.’ It fits right in with the sale. You’re not much of a salesman if you can’t get a sale with 0% interest rate,” Purcell says.

He says he faces two challenges when it comes to financing: bad customer credit and competition from nearby dealers who also finance through Sheffield.

“This summer, I’ve probably lost 10 or 12 sales because of bad credit. The sales are lost if Sheffield won’t finance. If a person doesn’t have good credit, there’s nothing much you can do,” he says.

Purcell describes the location of his nearest competitor this way: “I can throw a football and hit another dealership that uses Sheffield. It’s just part of the competitive world we live in. I try to work very hard at pickup and delivery. I try to give the best service, warranties and advice. I’m always going out to see my customers’ properties to see what kind of mower they need.”

Dealer View from Iowa

Javier Pelaez is DLL’s director of program management, food and agriculture.

Adam Heiken is co-owner of D&L Equipment, Kensett, Iowa. The dealership carries Kioti, Cub Cadet, Gravely, Grasshopper, Woods Equipment and other lines. About a year ago, Heiken began offering leasing arrangements for his rural equipment customers through DLL.

“Most of them never thought about leasing tractors. They think tractors cost about $5,000 and when they see they are more like $15,000, it comes as a big shock. So, leasing keeps them talking and presents a more affordable payment,” Heiken says.

“For those who want to update tractors in 3, 4 or 5 years, they like the idea of leasing. Others want to own the tractor and are not looking to update it in 4 years,” he says. Some don’t like the large payment at the end so they prefer to go with a purchase option.

Heiken says leasing has been critical to moving production tractors in the last 3 years. About half of his customer base are farmers, and many are familiar with the process and could use it to obtain smaller tractors. “It’s definitely worth looking into. It’s another tool. Right now the farm economy has everybody crunched, so we have to look at all options to make a sale,” he says. In the end, though, he follows what works best for his customers.