Last summer, the Equipment Dealers Assn. (EDA) and the Assn. of Equipment Manufacturers teamed up to survey their members about the levels of new and used inventory currently on the market. In order to see how the inventory situation has developed, a similar survey was conducted in July 2017. Here are some highlights:

Improved Perspective on Inventory Levels

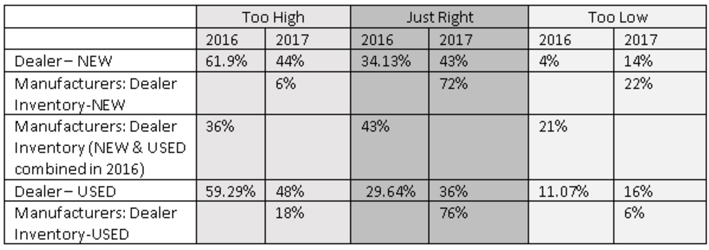

EDA’s dealership survey revealed that currently 43% of their dealers feel that their new equipment inventory is too high, 43% say it is just right and 14% feel it is too low. This is an improved perspective from 2016, where 62% thought that new equipment inventories were too high, and only 30% felt it was just right.

Dealers have a better perception of used equipment inventories this year as well. The percentage of dealers indicating that used equipment inventory is just right increased to 36% from 30% in 2016, and the number of dealers that feel used equipment inventory is too high dropped to 48% versus 59% last year. It therefore goes to reason that more dealers feel that used equipment inventory is too low, with 16% this year compared to 11% in 2016.

“Dealers have been more effective in managing their used inventory since the last survey. This is vitally important for the health of our dealers.” said Kim Rominger, president and CEO of EDA.

AEM’s survey indicates the majority of manufacturers feel that both new and used equipment inventories in their dealerships are currently just right at 72% and 76% respectively. This rates much higher than last year, when only 43% of manufacturers thought their dealership inventories were just right. When asked what the bigger issue is, used versus new equipment, the results basically show a 50/50% split.

Immediate Versus Long-Term Perspective

A difference in dealership and manufacturer perspective can be seen with regard to new equipment inventories in 2017. While 43% of dealers feel their new equipment inventories are too high, only 6% of manufacturers concur. Similarly, 48% of dealers feel their used equipment inventory is too high, and only 18% of manufacturers feel the same.

This plays out with a 29-40% difference between manufacturer and dealer opinion on 2017 dealership inventories being just right on the new and used equipment sides respectively. It must be noted that dealers have a more immediate standpoint and are likely considering inventories of multiple brands, whereas manufacturers are focused only on their brand and have a broader, longer term perspective.

The following chart indicates dealer and manufacturer sentiment toward new and used inventory levels in 2016 and 2017.

“The discrepancy in the results between dealer and manufacturer participants is not surprising based upon the disparity in dealership group size and the year that we have had,” said Rominger. “Large agricultural dealers tend to have higher value late model large used equipment without the diversity of the market enjoyed by small agricultural equipment dealers. Larger agricultural equipment seems to be moving more slowly and is requiring more effort or concessions on price than we are seeing in the small agricultural equipment arena. In addition to these issues, we continue to see the commodities economy struggle, and many areas of the country are coping with severe weather issues. In some regions, heavy rainfall has delayed or impeded planting altogether, while other regions are battling a debilitating drought. On the other hand, some regions are projecting record crop years, and dealerships which cater to specialty crop growers are largely on-target with their budget forecasts. While dealers are taking the survey with their own “micro” perspective, based upon their region and target customer, manufacturers seem to feel more balanced with respect to inventory, overall.”

Favorable Trends

Compared to the previous year, most manufacturers (44%) feel their inventories are staying about the same. When asked about their dealer inventories compared to last year, 60% say that overall they also stayed the same.

“We still see major discrepancies between the sale of large, high horse power tractors and combines versus smaller tractors. Sales for tractors under 40HP are up 11% from last year, while sales for 100HP+ tractors are down 15.5%. Combine sales are down 5.7% from last year. And with no big changes foreseeable in commodity prices, no big changes in production agriculture equipment purchases are anticipated either," said AEM Senior Vice President and Ag Sector Lead Curt Blades.

The short term indicates a more positive trend towards a reduction of inventories at both the dealer and the manufacturer level. Over the last three months, the majority of dealers indicate a decrease in both new (45%) and used (40%) equipment inventories. Another 34% (new) and 37% (used) indicated their inventories remaining stable. The majority of manufacturers (53%) indicate that inventories at their facilities have remained stable over the past three months, with 24% indicating that their inventories are decreasing.

“Manufacturers, however, are feeling better about their own inventory levels as well as that of their dealers’,” said Blades. “Many of them have focused considerable efforts towards scaling those inventories down —- from adjusting production levels to offering discount programs, extending marketing campaigns and increasing the number of retail program offerings. Some have hired new supply chain professionals to be smarter about safety stock procurement. Others are working more closely with their customers to get better purchasing forecasts. Some approaches have been more successful than others for different manufacturers, but overall these efforts are beginning to pay off.”

About EDA

Founded in 1900, the Equipment Dealers Assn. (EDA) — formerly known as the North American Equipment Dealers Assn. (NAEDA) — is a non-profit trade organization that represents approximately 4,500 retail dealerships across the United States and Canada. Our mission at EDA is simple: we are committed to building the best business environment for equipment dealers.

About AEM

AEM is the North American-based international trade group providing innovative business development resources to advance the off-road equipment manufacturing industry in the global marketplace. AEM membership comprises more than 950 companies, including 450 in the agriculture sector, and more than 200 product lines in the agriculture, construction, forestry, mining and utility sectors worldwide. AEM is headquartered in Milwaukee, Wisconsin, with offices in Washington, D.C.; Ottawa, Canada; and Beijing, China.