For dealers who focus on the rural lifestyle market, spotting economic patterns that provide data for planning or support marketing and sales efforts isn’t as clear cut as it is for retailers whose main customers are production farmers. Dealers handling big ag equipment have very tangible and obvious indicators — from crop and cash receipts, commodity prices and net farm income — to help guide them in anticipating trends and meeting current demand for farm machines and implements.

Because the sales of rural lifestyle-type equipment and products tends to be tied to general consumer trends, dealers need to look more closely at a different set of leading and/or lagging indicators to spot emerging opportunities or confirm already emerged patterns.

Investopedia defines these as follows: Leading indicators often change prior to large economic adjustments and, as such, can be used to predict future trends. Lagging indicators, however, reflect the economy’s historical performance and changes to these are only identifiable after an economic trend or pattern has already been established.

As a rural lifestyle dealer, which indicators are important for you to pay attention to?

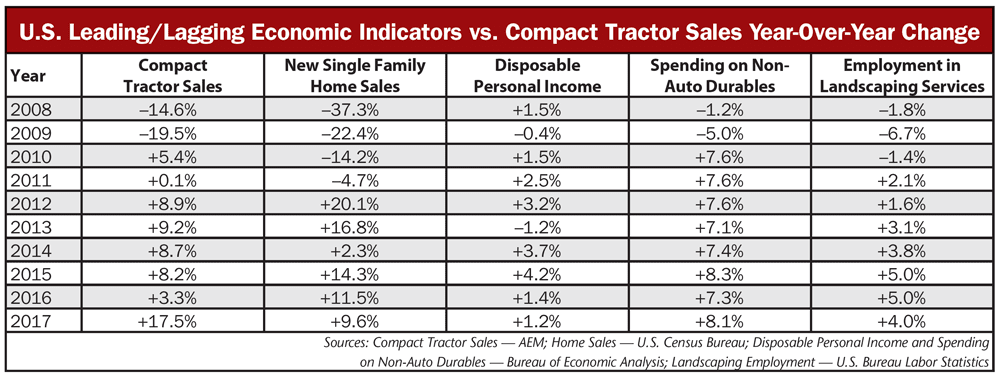

Each year, John Deere publishes a series of Fact Books that provide a wealth of information on its business, as well as the markets it serves. One of them is called “Turf Data.” It provides historic and current data for several important indicators for its turf market segment. Among these are sales of existing single family homes, sales of new single family homes, Disposable Personal Income, Spending on Non-Auto Durables, Employment in Landscaping Services and Employment in Golf Courses and Country Clubs. (Deere is a major supplier of golf course maintenance equipment.)

The adjacent table shows the year-over-year changes in four of these leading/lagging indicators for the 10 years between 2008-17 (2018 data is not yet available) and compares them with the year-over-year changes in the sales of tractors under 40 horsepower. This provides an easy comparison of the ups and downs of each indicator in the sales of small tractors, which most rural lifestyle dealers are familiar with.

Of course, the numbers shown are countrywide, but they are also available on a regional basis and, in some cases, on a state-by-state basis. Dealers who want to take a step up in their annual forecasting skills should find this type of data helpful.

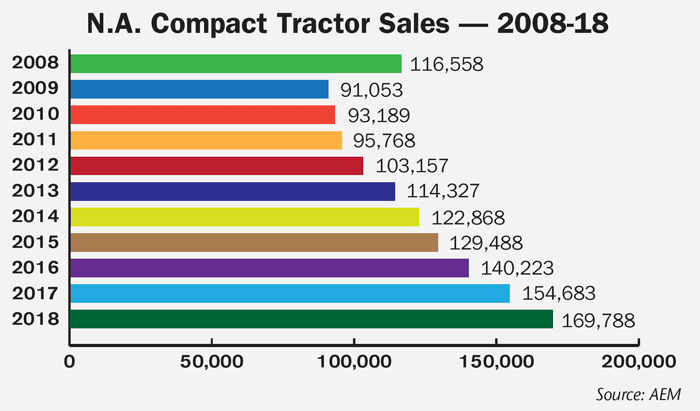

2018 Compact Tractor Sales Another Record Breaker

Responding to the most recent Ag Equipment Intelligence Dealer Sentiments & Business Conditions Update survey, one dealer summed up the state of the rural lifestyle market in 2018: “Commercial sales are way up, specifically for less than 100 horsepower tractors.” The numbers coming from the Assn. of Equipment Manufacturers back up this dealer’s commentary, particularly in the sales of under 40 horsepower tractors. According to the latest AEM numbers, North American sales of compact tractors were 169,788, up 8.8% in 2018 and up more than 80% when sales bottomed out 2009.