Following a challenging year in 2024, rural lifestyle dealers are maintaining an optimistic outlook for business in the year ahead. According to the 2025 Rural Lifestyle Dealer Business Trends & Outlook report, the majority of dealers are forecasting revenues to be as good or better in 2025 compared to last year. That said, while 2024 revenues didn’t live up the dealers’ forecasts for the year, 84.9% of dealers did report they were profitable in 2024. When it comes to which products dealers expect to have success with in 2025, ATVs and zero-turn mowers topped the list.

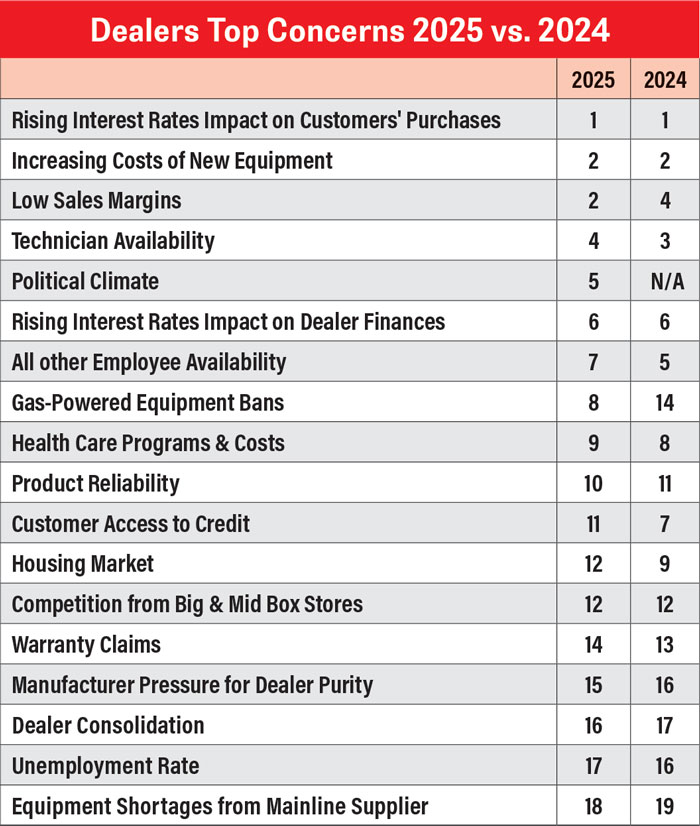

Despite the recent interest rate cuts the Federal Reserve announced last fall, rising interest rates once again topped the list of dealers’ concerns. The rising cost of new equipment and low sales margins also top issues weighing on dealers’ minds for the year. Dealers’ wholegoods inventory turns held relatively steady in 2024 compared to 2023.

Revenue Forecasts Improve

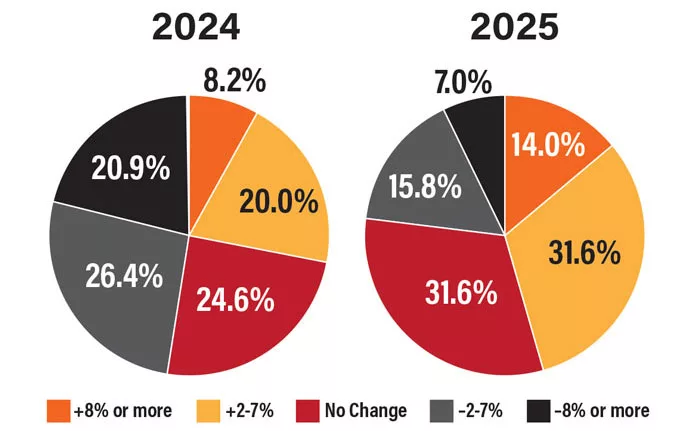

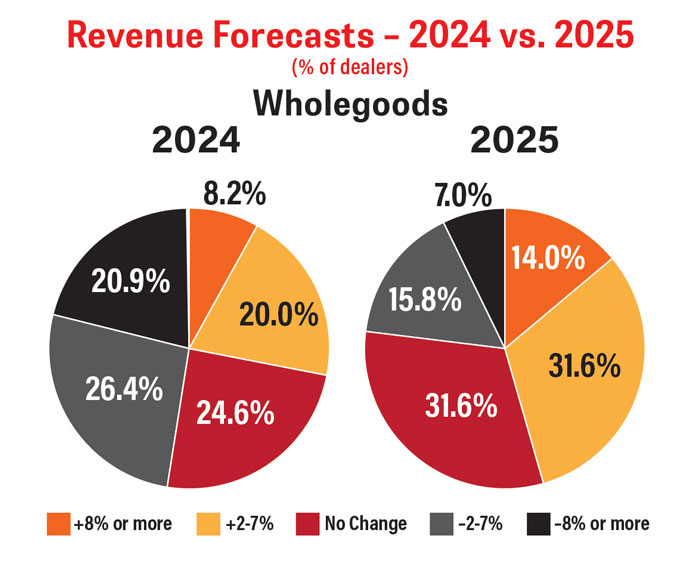

Looking at their forecasts for 2025, dealers are more optimistic about their chance for improving revenues than they were in their 2024 forecasts. Just over 77% of dealers expect their wholegoods revenues to be as good or better than 2024, with 31.6% forecasting growth of 2-7%. Last year, 52.8% of dealers were forecasting wholegoods revenues to be as good or better than 2023.

Get the Full Report: 2025 Rural Lifestyle Dealer Business Trends & Outlook

Gain exclusive insights into dealer expectations, challenges, and opportunities in the year ahead. This in-depth report uncovers historical and current dealer sentiment, helping you better understand how to serve the rural lifestyle market. Click here to access the full report.

For the year ahead, 14% of dealers expect their wholegoods revenue to be up 8% or more. Another 31.6% of dealers are expecting revenue from wholegoods sales to be in line with 2024. When it comes to dealers who forecast a revenue decline, 15.8% expect wholegoods revenues to drop 2-7% (vs. 26.4% who called for this decline in 2024) while 7.0% are forecasting a decline of 8% or more vs. 20.9% in 2024.

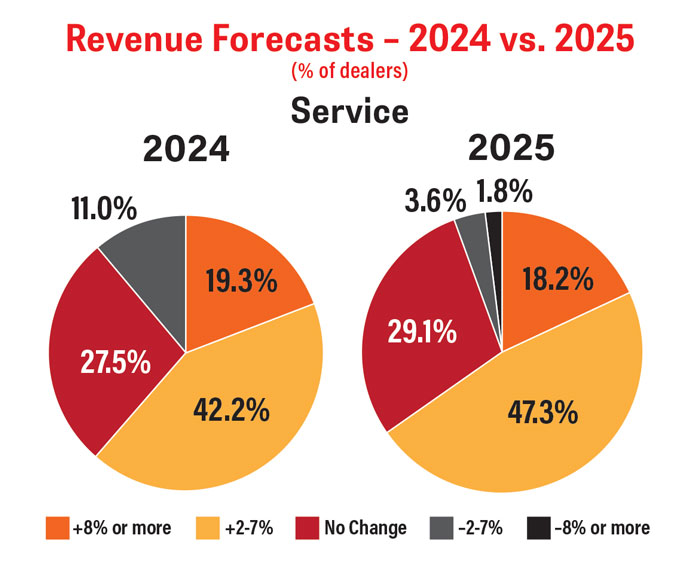

Regarding service, nearly 95% of dealers reported they expect their revenue to be as good or better than 2024 vs. 89.0% who said the same the previous year. Of those forecasting service revenue growth, 47.3% expect revenues to be up 2-7% vs. 42.2% in the 2024 report. The percentage of dealers expecting service revenue to be up 8% or more dropped about a point to 18.2% vs. 19.3% in 2024. In the 2024 report, no dealers were calling for a decline of 8% or more, but this year just shy of 2% of dealers are calling for this level decline. Meanwhile, 3.6% of dealers expect service revenue to be down 2-7% in 2025 vs. 11.0% in 2024.

Dealers are the most optimistic about their parts revenue for 2025, with 96.4% expecting revenues to be as good or better than in 2024. Of that, 58.2% are forecasting parts revenue to be up 2-7% vs. 50.5% who made the same forecast for 2024. Nearly 13% of dealers expect their parts revenue to improve 8% or more compared to 11.0% in 2024. Fewer dealers are calling for parts revenues to be down in 2025 than did last year. Of those forecasting a decline, 3.6% expect revenues to be down 2-7% (6.4% in 2024) and 1.8% expect a decline of 8% or more (0.9% in 2024).

2024 Revenue Estimates vs. Forecasts

Dealers’ forecasts last year were more positive than the results they ultimately reported. According to the latest survey, just 39.3% of dealers reported their wholegoods revenue was as good or better than it was in 2023. Going into 2024, 52.8% of dealers were forecasting their wholegoods sales would be as good or better than 2023. Breaking it down, 10.7% of dealers reported 2024 wholegoods revenues were up 8% or more compared to 8.2% who forecast that level of growth heading into the year. Fewer dealers saw growth of 2-7% in 2024 (14.3%) than the percentage who forecast that level of growth (20.0%). More dealers saw wholegoods revenues decline when all was said and done than forecast it going into 2024 — 41.1% reported 2024 revenues down 2-7% over 2023 compared to 26.4% who forecast their 2024 revenues would be down this much.

On the service side of the business, dealers forecasts didn’t live up to what their year-end estimates for revenues were in 2024. Heading into the year, 42.2% of dealers expected service revenues to be up 2-7%. According to the latest survey, 29.6% of dealers reported their service revenue was up 2-7% over 2023. Another 13.0% of dealers reported revenues were up 8% or more, down from the 19.3% who forecast that level of growth heading into 2024. More dealers, however, reported flat service revenues than had forecast little or no change — 42.6% vs. 27.5% who forecast flat revenues at the start of 2024.

Looking back on 2024, 37.0% of dealers said their parts revenue was up 2-7% vs. 2023. This compares to 50.5% of dealers who had forecast this level of growth heading into 2024. More dealers (13.0%) reported their parts revenue was up 8% or more in 2024 than had forecast growth of that level at the start of the year (11.0%). Dealers who forecast flat parts revenues were pretty spot on, with 31.2% forecasting little or no change at the start of the year vs. 31.5% who reported those results for 2024.

Best Bets for Improving Sales

When asked what equipment they saw as their “best bet” for improving unit sales in 2025, in the #1 spot 84.4% of dealers pointed to ATVs, up from #5 in 2024. Spraying equipment came in at #2 (83.7%), up 4 spots from 2024, followed by skid-steer loaders at #3 (83.3%) up from #20 last year. Compact excavators (82.5%) also made a big jump, coming in at #4 and up 16 spots from last year’s report. Rounding out the top 5 was post-hole diggers with 82.2% of dealers expecting their sales to be as good or better in 2025.

When you take out the little or no change responses and look only at growth or decline, zero-turn mowers top the list with 55.1% of dealers forecasting their unit sales will be up at least 2% in 2025, up from 50.5% who had the same forecast for 2024. Utility tractors are next on the list with 42.6% of dealers forecasting unit sales growth of 2% or more vs. 25.3% last year. Rotary cutters round out the top 3 with 41.3% of dealers expecting growth vs. 38.9% in 2024.

Top Concerns

The impact rising interest rates will have on customers’ purchases once again tops the list of dealers’ top concerns, with 98.0% of dealers saying they were either concerned or most concerned. The increasing cost of new equipment came in at #2 on the list with 50.0% of dealers saying they were most concerned and 46.0% saying they were concerned. This was tied with low margins (46.0% most concerned, 50.0% concerned). Technician availability and political climate round out the top 5 for dealer’s concerns.

Brands & Products

A little over a third of dealers (37.3%) say customers have a specific product or brand in mind almost all of the time when they come to the dealership. Another 43.1% of dealers say customers know what they’re looking for some of the time, while 15.7% say this is the case almost always. Just shy of 4% of dealers say customers hardly ever have a specific product or brand in mind when they come into the store.

Over half of dealers (52.9%) say that customers take their product recommendations most of the time, down from 69.9% last year and 71.6% in 2023. But, the percentage of dealers who say customers almost always take their recommendations bounced back after falling in 2024. This year, nearly a quarter of dealers (23.5%) said customers almost always take their advice compared to about 13% in 2024.

When asked where they’re looking to expand their product mixes, 40-100 horsepower tractors and zero-turn mowers topped the list with 53.9% of dealers looking to expand in those categories for 2025. Skid-steer loaders, the top product area to expand for 2024, was third on the list this year followed by <40 horsepower tractors and compact excavators.

That said, only 22.0% of dealers say they expect to add an equipment line in the next 2 years, down 20 percentage points from the 2024 report.

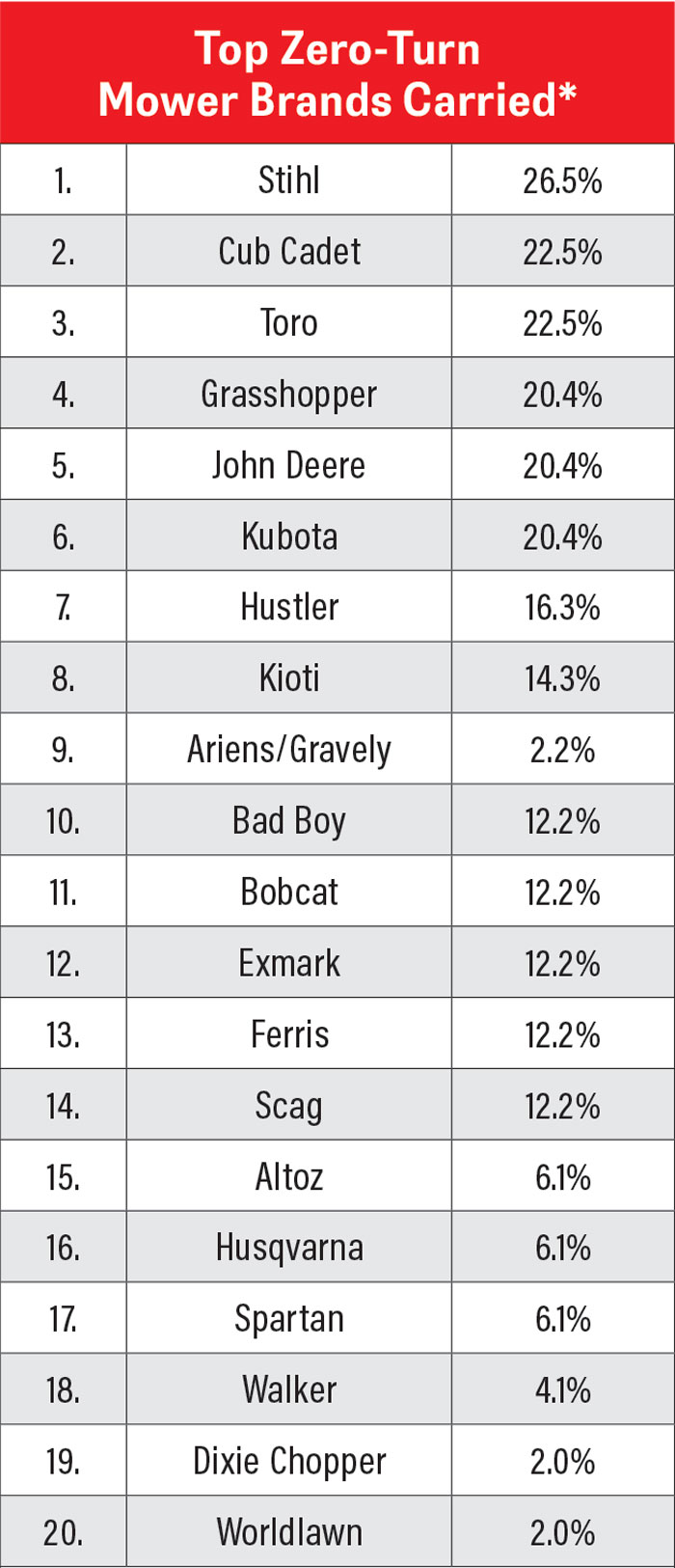

*Dealers could select multiple brands, so percentages equal more than 100%. Source: Rural Lifestyle Dealer Business Trends & Outlook surveys

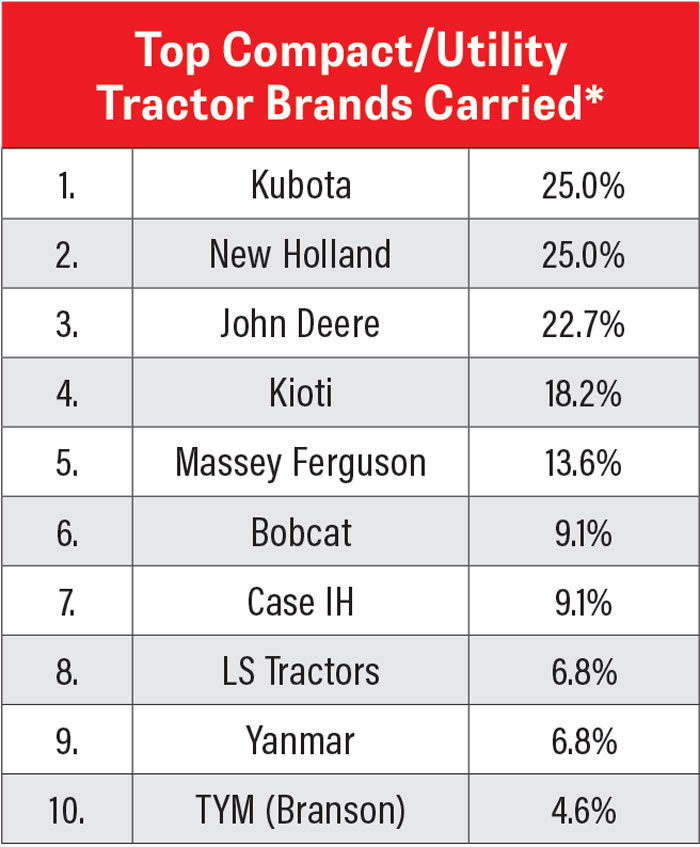

*Dealers could select multiple brands, so percentages equal more than 100%. Source: Rural Lifestyle Dealer Business Trends & Outlook surveys

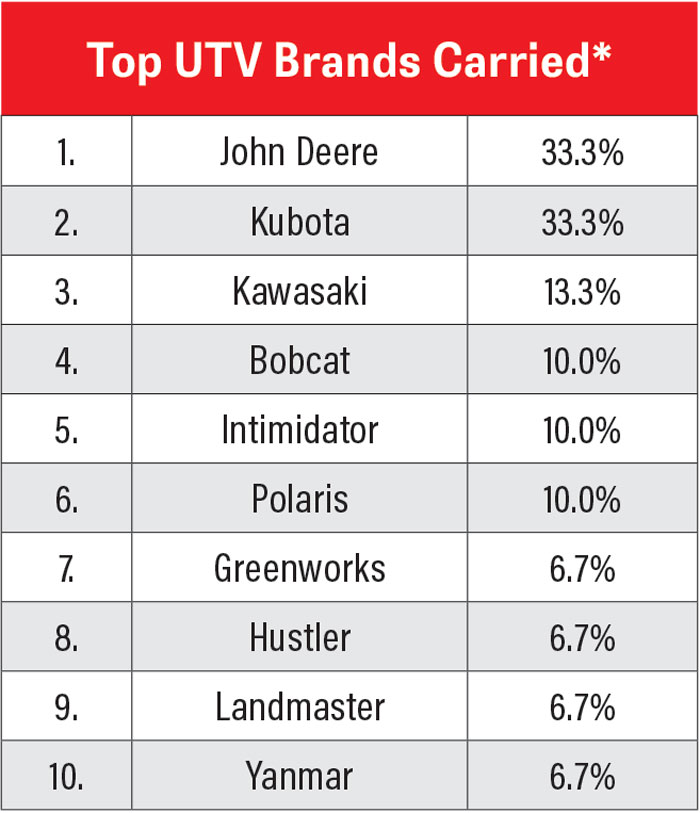

*Dealers could select multiple brands, so percentages equal more than 100%. Source: Rural Lifestyle Dealer Business Trends & Outlook surveys

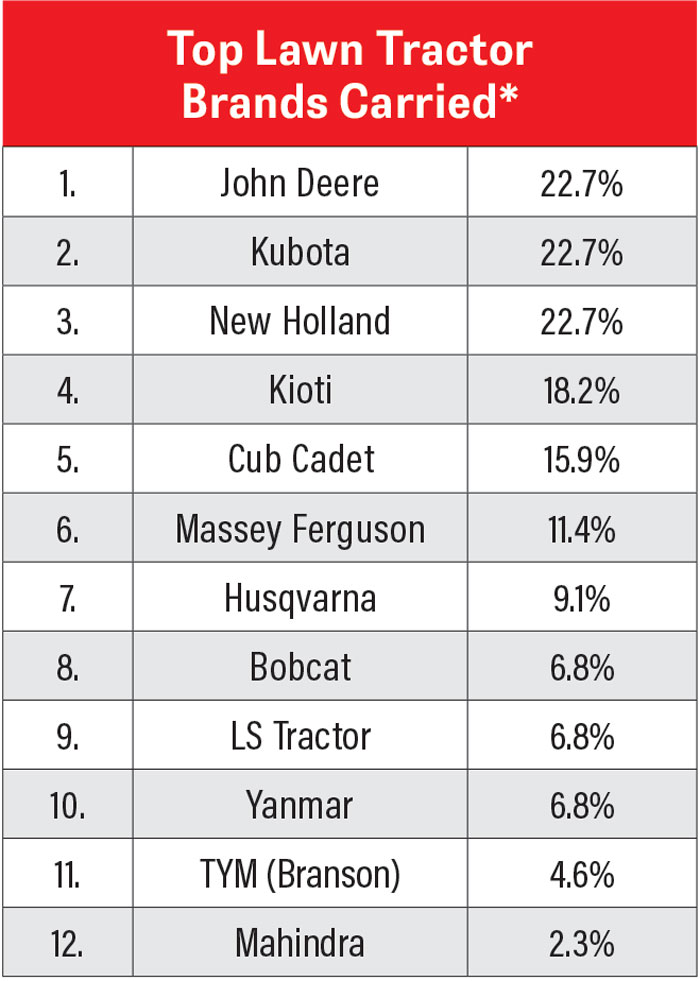

*Dealers could select multiple brands, so percentages equal more than 100%. Source: Rural Lifestyle Dealer Business Trends & Outlook surveys