The trend toward moderated optimism for the rural equipment market that showed up in 2019 looks to continue this year, with aftermarket revenue and zero-turn mowers being growth drivers in 2020. This is based on responses from dealers across North America in Rural Lifestyle Dealer’s 12th annual Dealer Business Trends & Outlook Report.

The moderation needs to be placed into context, however, as the rural equipment market remains strong with about 85% of dealers expecting 2020 to be a good year.

The Business Trends & Outlook Report is the only one of its kind to analyze the rural lifestyle equipment niche. For some, the segment helps balance out declines in the ag equipment market. And for many, big changes happening in technology such as battery-powered equipment, autonomous mowers and connected devices will break open new sales opportunities.

Analyzing Data

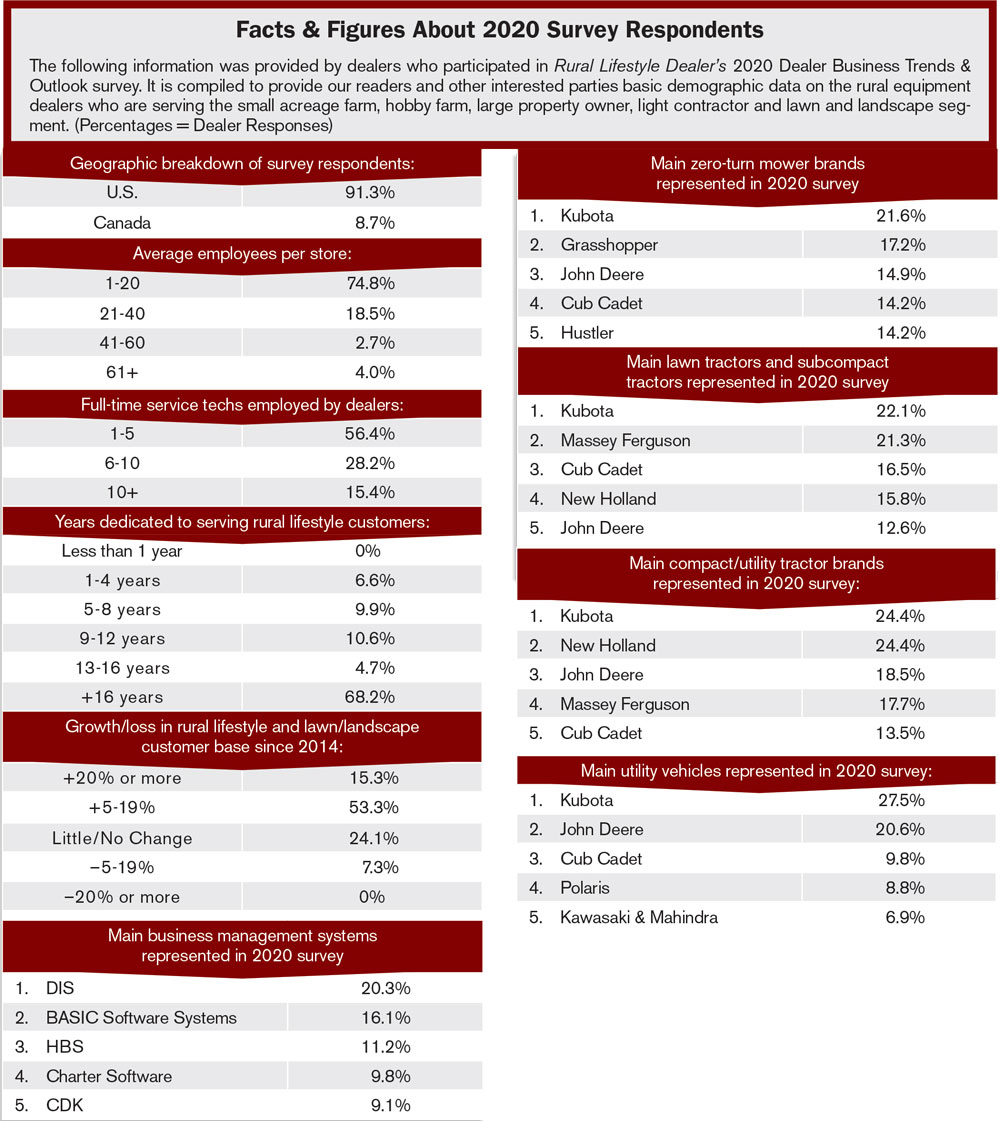

Let’s get to the numbers. About 68% of the respondents have been serving the market for more than 16 years. They report that the niche continues to expand with about 53% saying their market has grown 5-19% in the last 5 years. (See more demographic data in the table at the bottom of this page.)

Dealer Takeaways

- About 85% of North American rural equipment dealers say 2020 will be as good as or better than 2019. About 91% say aftermarket revenue will be as good as or better than last year.

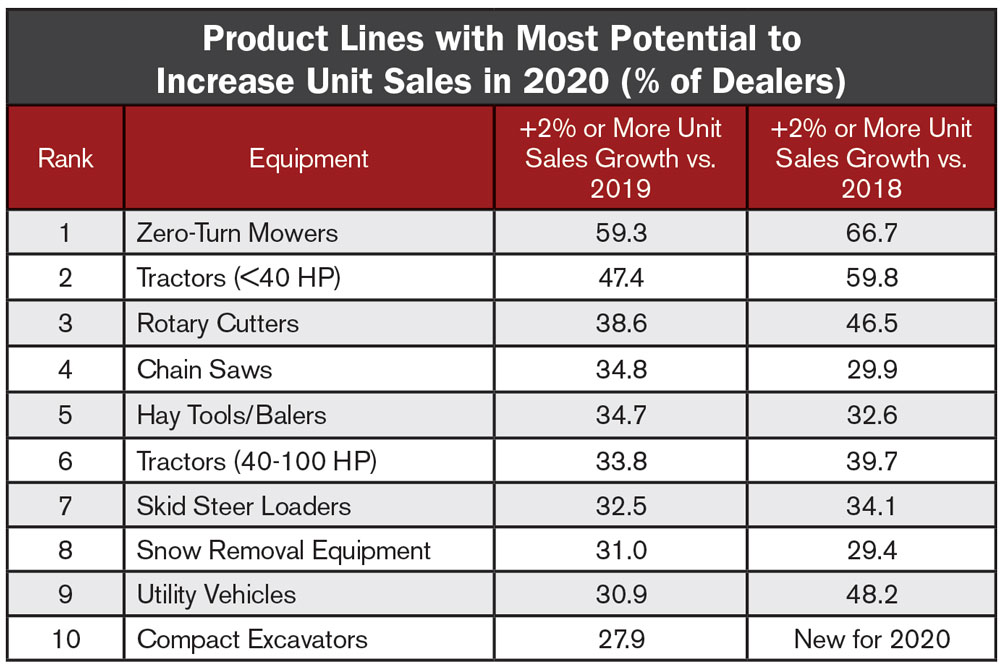

- The top 5 categories driving unit sales growth in 2020 are zero-turn mowers, tractors under 40 horsepower, rotary cutters, chain saws and hay tools/balers.

- Finding good employees, healthcare programs and costs and low sales margins are the top 3 issues dealers are most concerned about.

- More than 53% of dealers say their market has grown 5-19% in the last 5 years and more than 16% say they’ve experienced growth of 20% or more. About 68% of dealers have been serving rural lifestyle customers for more than 16 years.

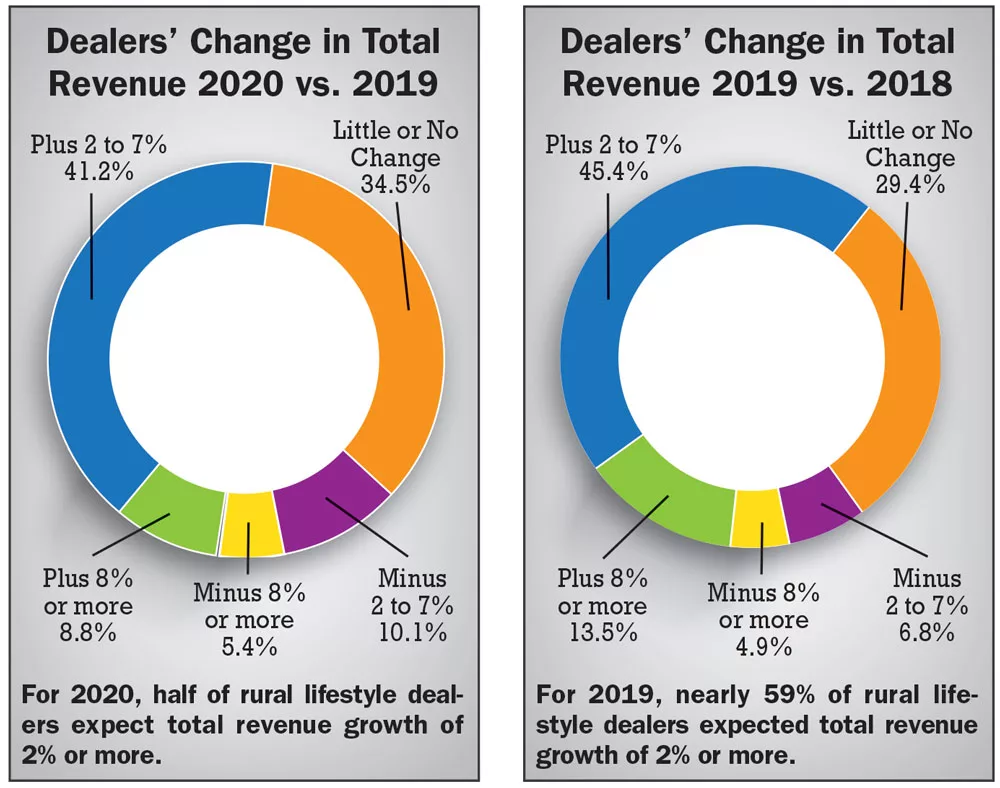

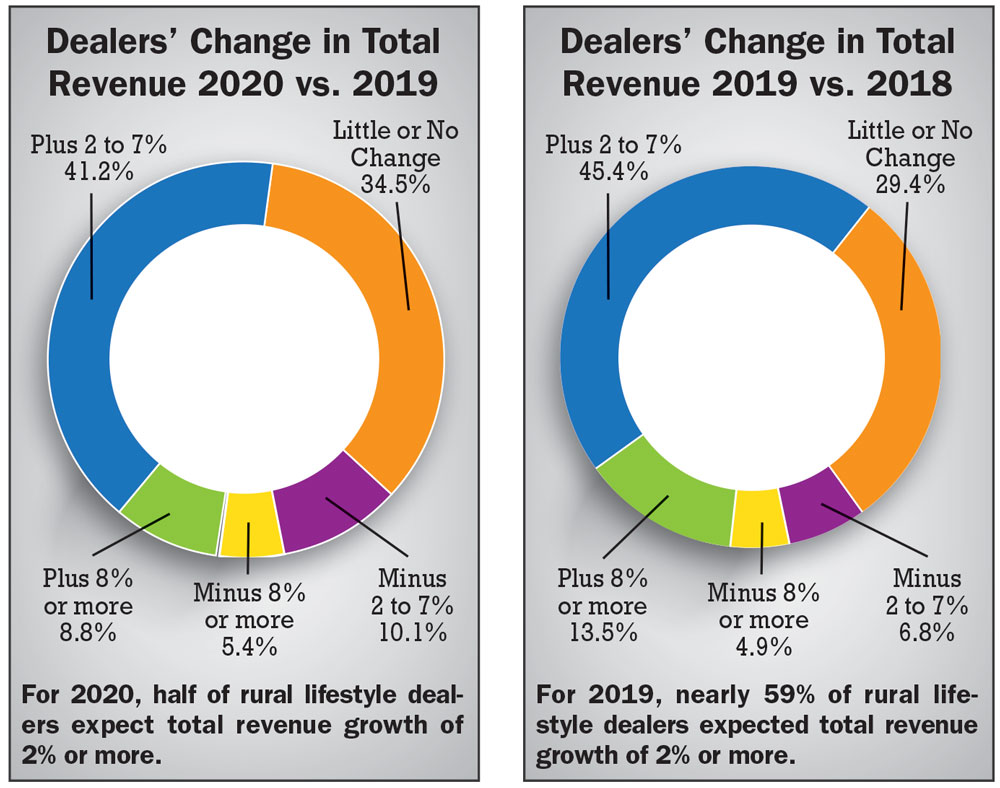

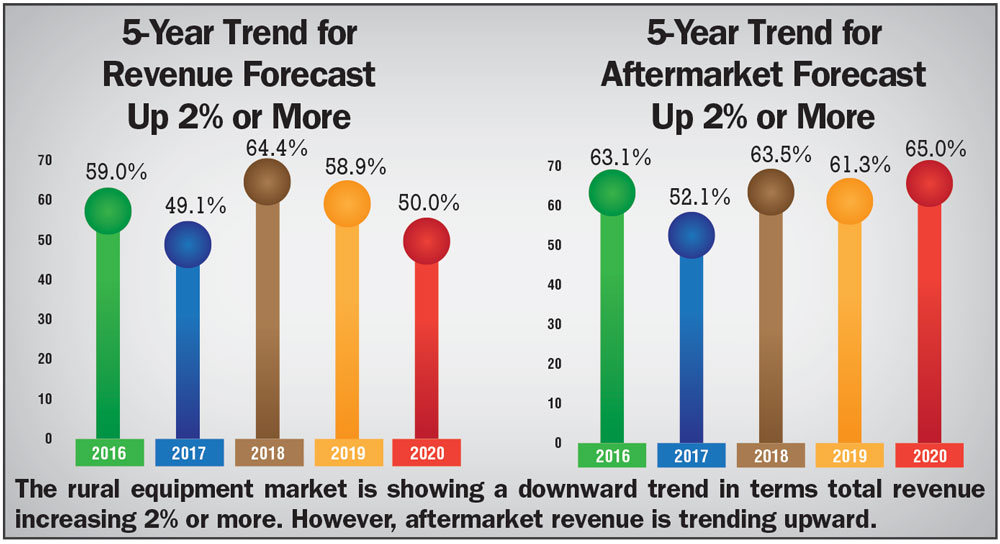

Overall, about 85% of rural equipment dealers expect total revenue in 2020 to be as good as or better than 2019. That compares with 88% in last year’s survey. Broken down further, half expect total revenue to increase 2% or more; about 35% expect similar numbers as last year; and nearly 16% expect total revenue to decline by 2% or more. (See the charts below.)

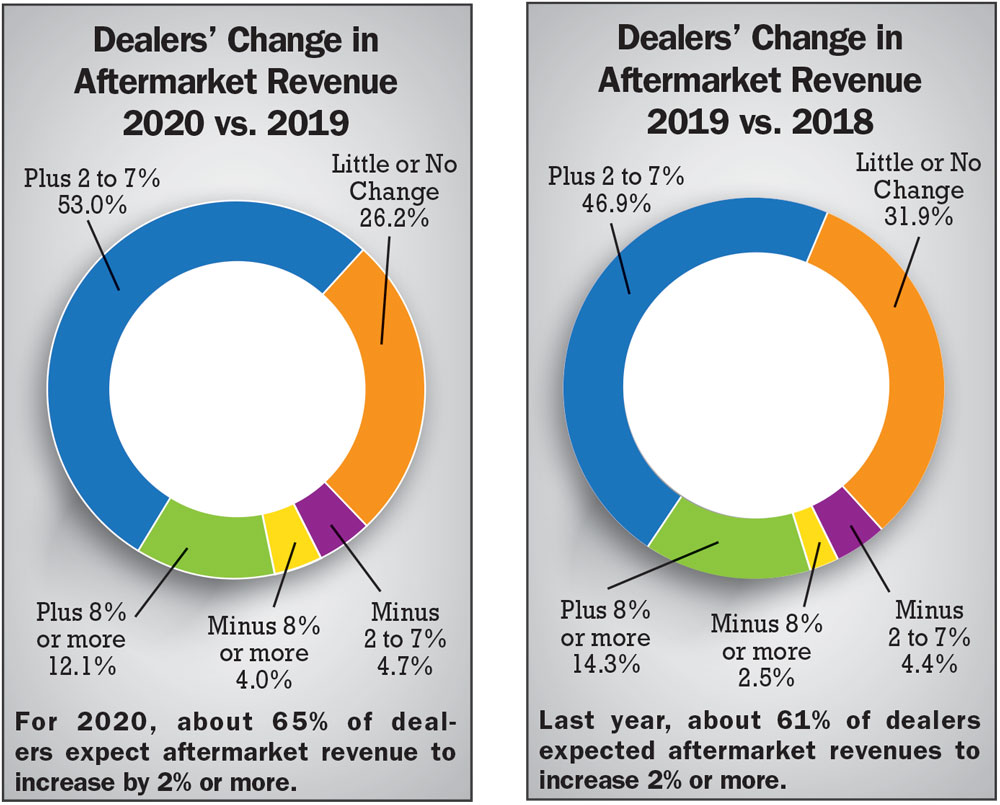

Aftermarket revenues are typically forecast higher and that bore out again this year. About 91% of dealers expect aftermarket revenue in 2020 to be as good as or better than 2019. That compares with 93% in last year’s survey. Broken down further, about 65% expect aftermarket revenue to increase 2% or more, 26% expect similar numbers as last year and about 9% expect aftermarket revenue to decline 2% or more. (See the charts below.)

The 5-year trend for total revenues is trending downward, while the 5-year trend for aftermarket revenues is trending upward. (See the charts below.)

Here’s another comparison using the weighted average, where the increasing revenue figure is compared against decreasing revenue. A larger number indicates higher optimism. The weighted average for total revenue in 2020 is 1.67 compared with 2.43 in 2019. The weighted average for aftermarket revenues in 2020 is 2.82 compared with 2.86 for 2019.

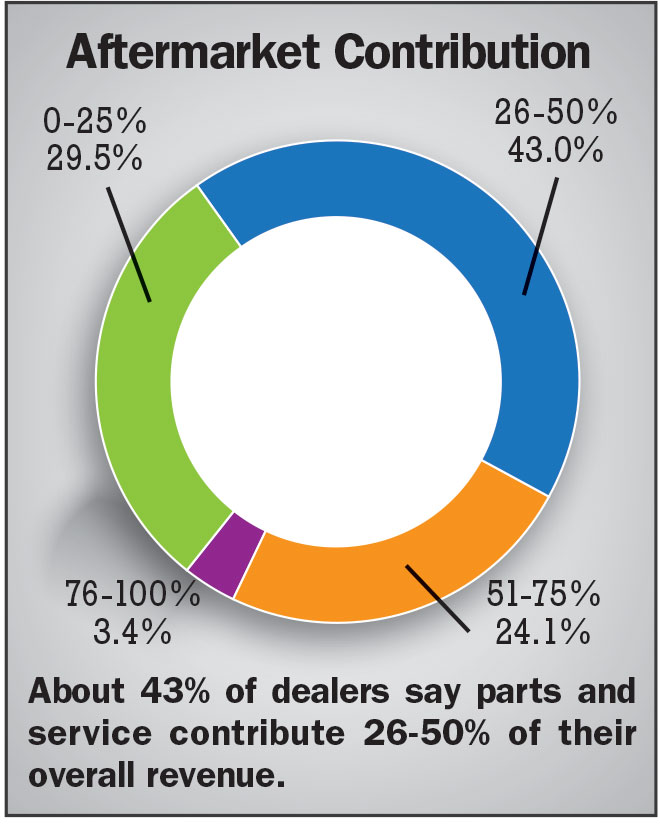

About 43% of dealers say their parts and service departments contribute 26-50% of their overall revenue. (See the chart, “Aftermarket Contribution” below.)

Watch for More Analysis

A special report will post soon on www.RuralLifestyleDealer.com Also, watch for registration details for an interactive webinar.

What’s Driving the Segment?

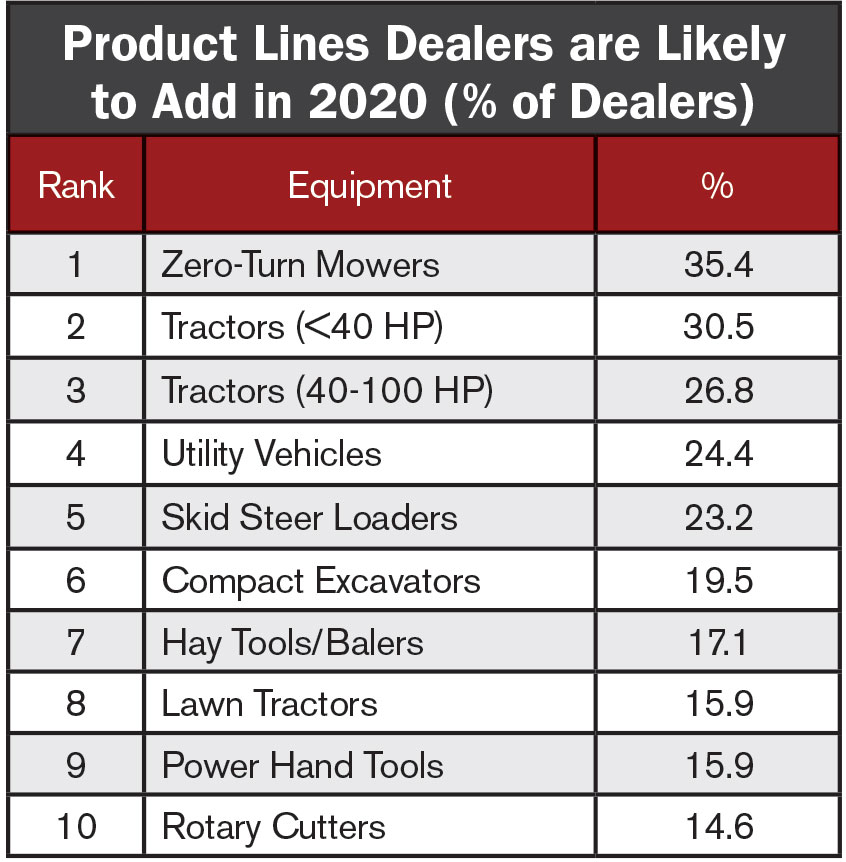

The top 5 categories driving unit sales growth in 2020 are zero-turn mowers, tractors under 40 horsepower, rotary cutters, chain saws and hay tools/balers. Zero-turn mowers have topped the list for the last 5 years and this year, nearly 60% of dealers expect unit sales to increase 2% or more. That optimism is down slightly from last year when 66.7% of dealers expected similar increases of unit sales. (See the table “Product Lines with Most Potential to Increase Unit Sales in 2020” below.)

There have been some shifts among the categories in unit sales projections as utility vehicles dropped from third last year to ninth this year. Chain saws moved up to fourth from the 11th position last year.

Compact excavators were added to the list of categories this year and they ranked 10th out of the 27 categories surveyed. Nearly 28% of dealers expect unit sales of compact excavators to increase 2% or more this year.

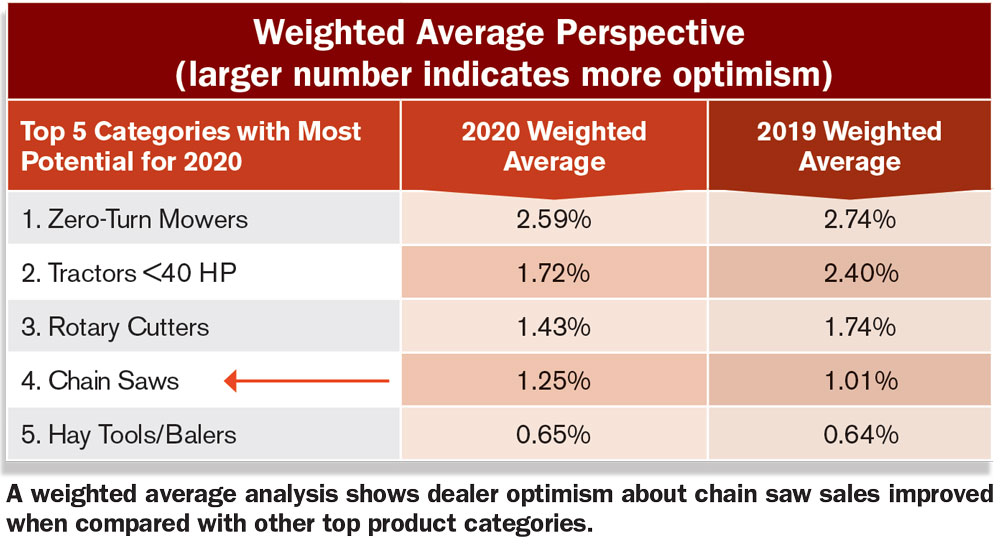

The weighted average perspective shows dealers are especially optimistic about the sales of chain saws. (See the chart “Weighted Average Perspective” below.)

Expanding Lineups

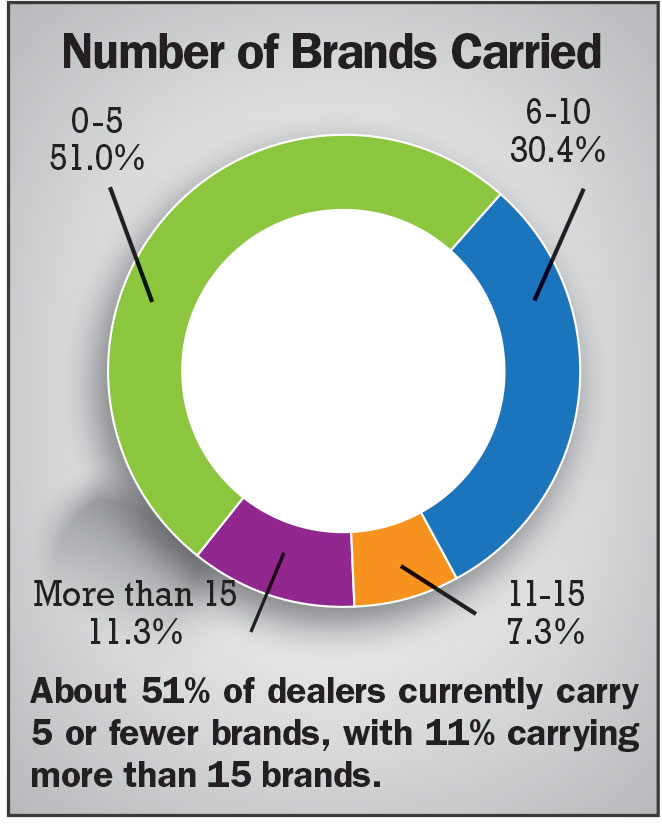

Several new questions looked at dealers’ current lineups and plans for the next 2 years. About 51% of dealers currently carry 5 or fewer brands, with 11% carrying 15 or more brands. (See the chart “Number of Brands Carried” below.) About 75% of dealers said they did not expect to add an equipment line this year.

Zero-turn mowers top the list of product lines dealers will be adding, with about 35% adding the equipment in 2020. Rounding out the top 5 regarding products being added are tractors under 40 horsepower, tractors 40-100 horsepower, utility vehicles and skid steers. Those same categories made up the top 5 in last year’s survey, with zero-turn mowers moving up from the fourth spot. (See the table “Product Lines Dealers are Likely to add in 2020” below)

The new category measured this year, compact excavators, placed sixth. Power hand tools moved up on the list to 9th this year from 19th in last year’s survey

Setting Policies

This year, dealers responded to several new questions about business operations and Sara Hey, business development manager for Bob Clements Intl., offers her perspective.

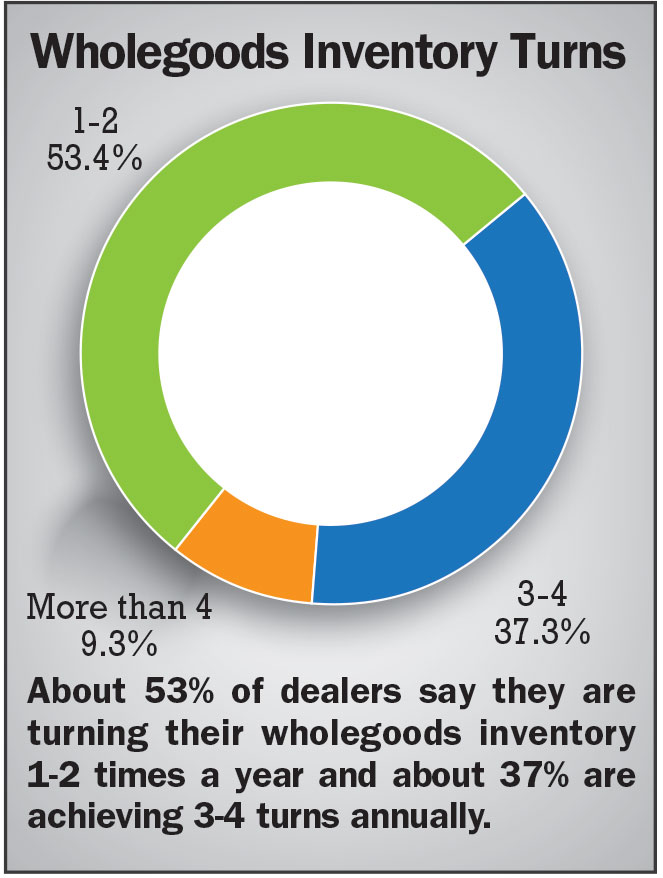

Regarding wholegoods inventory, about 53% turn wholegoods 1-2 times a year and about 37% achieve 3-4 turns. (See the chart, “Wholegoods Inventory Turns” below.)

“Rural lifestyle dealers should be turning their equipment 2 times a year, on average,” says Hey.

Regarding the number of brands they carry, about 51% of dealers carry 5 or fewer; 30% carry 6-10; 7% carry 11-15 brands; and about 11% carry more than 15. (See the chart, “Number of Brands Carried” above.) “It’s not necessarily about the number of lines (while 15 is a lot). It’s about not having competing lines. We want our lines to be complementary,” says Hey.

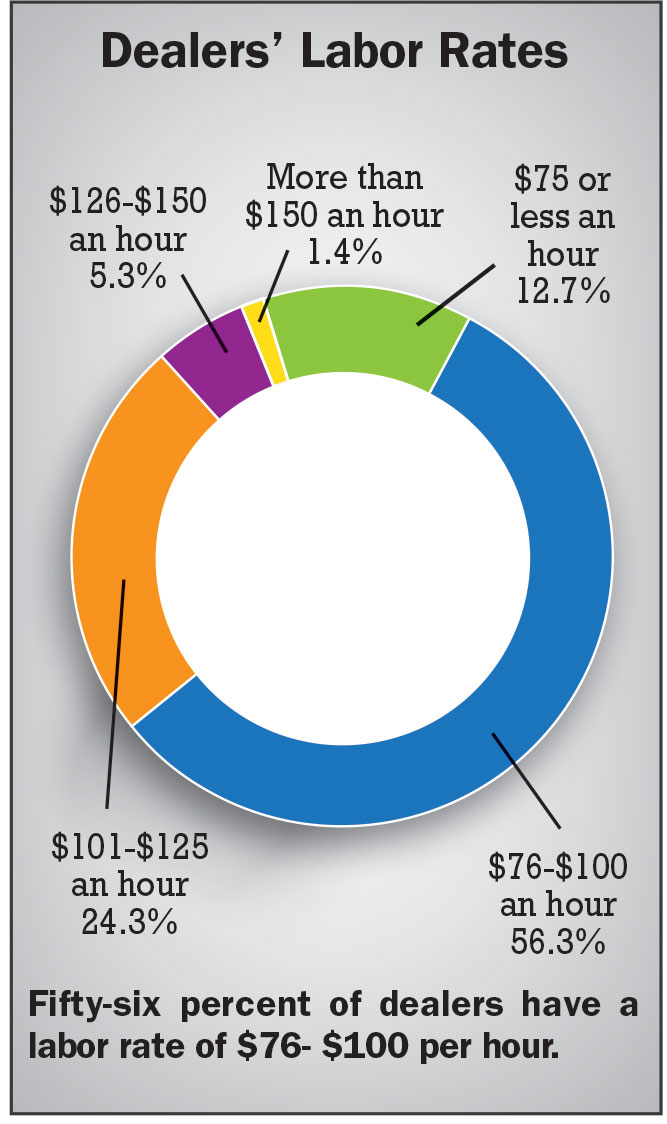

Dealers shared their labor rates with 56% charging between $76 and $100 per hour, compared with 63% in last year’s survey. Nearly 24% are charging $101-125 an hour, matching last year. (See the chart “Dealers’ Labor Rates” below).

Hey says this about labor rates, “This is dependent upon the part of the country that they are in. We encourage dealers to be about 10% below the local Ford dealers’ labor rate. Dealers should ask themselves how much it costs to hire a good technician. I would say that most of our dealers are between the mid-$80s and $110 range,” she says.

Promoting Brand

Brand awareness and reputation are other intangible influencers of profitability as competition is only getting stronger from online retailers, big box stores and other dealerships.

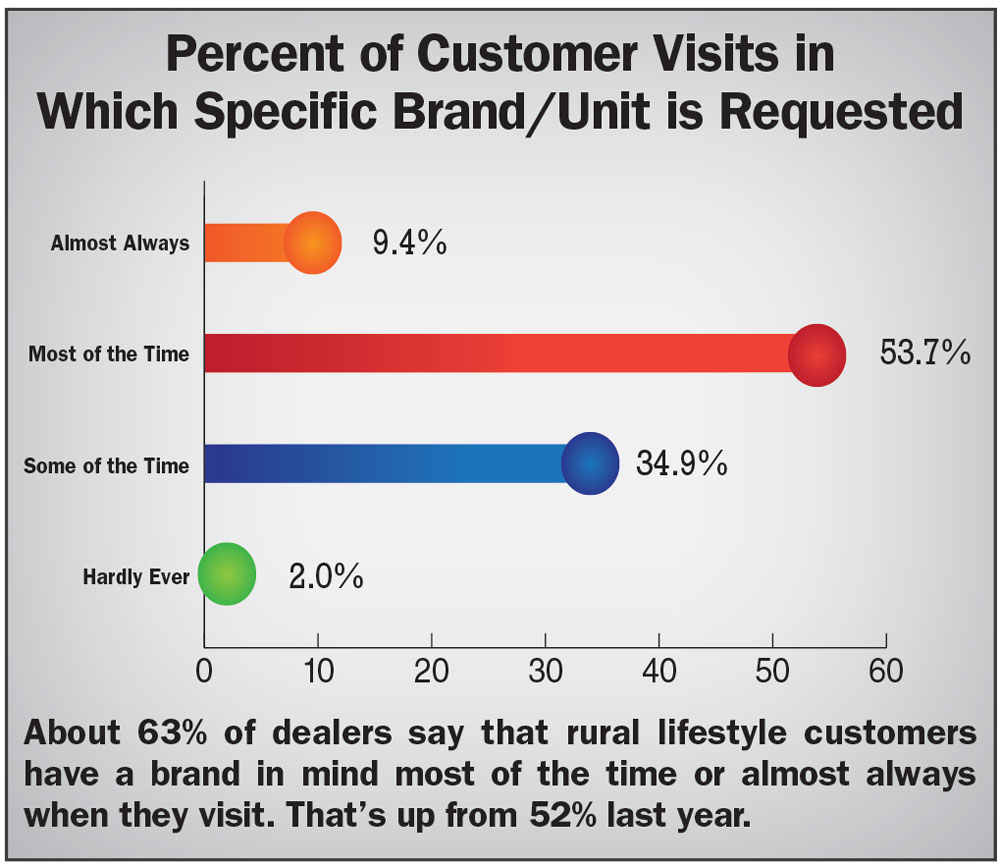

Dealers indicate a boost in brand awareness. About 63% of dealers say that rural lifestyle customers have a brand in mind most of the time or almost always, up from 52% last year. (See the chart “Percent of Customer Visits in Which Specific Brand/Unit is Requested” below.)

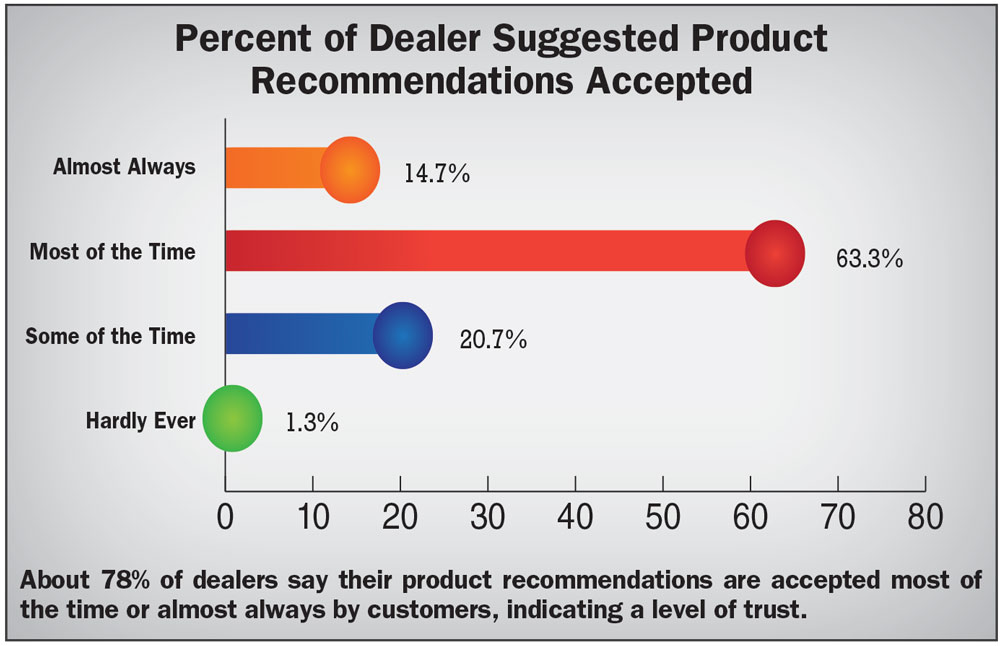

Dealers are capitalizing on this opportunity, adding in their expertise to earn customers. About 78% say their product recommendations are accepted most of the time or almost always. This is holding steady as 77% of dealers indicated this last year. (See the chart “Percent of Dealer Suggested Product Recommendations Accepted” below.)

Influencing Factors

Dealers are investing in improving their service departments, with about 57% expecting to modernize this year. That about matches last year’s survey.

About 47% expect to improve their retail spaces this year, again in line with last year. Regarding investments in business systems, about 30% saying they are making investments this year compared with 37% last year.

The survey looks at other factors influencing revenues, including rental and financing. About 41% of dealers say they offer rental equipment, down from the 45% reported last year. The top 5 product categories rented are skid steer loaders, compact excavators, tractors 40-100 horsepower, tractors less than 40 horsepower and zero-turn mowers.

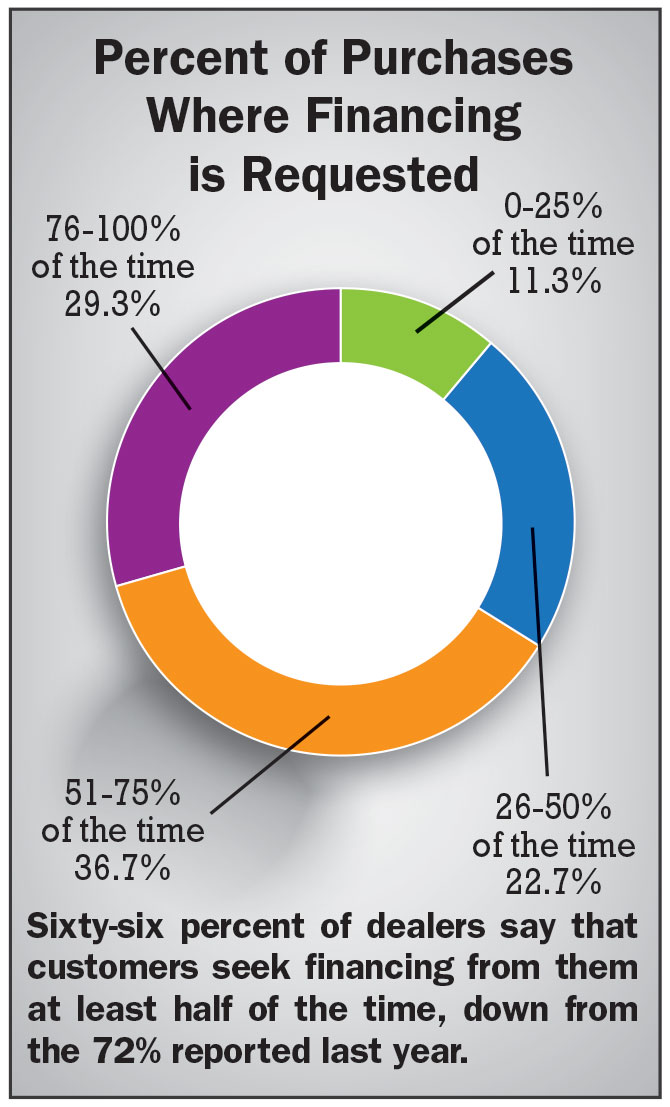

Sixty-six percent of dealers say customers seek financing from them at least half of the time, down from the 72% reported in last year’s survey. (See the chart “Percent of Purchases Where Financing is Requested” below.)

On a macro level, manufacturer research & development will drive excitement in the industry. Alyn Brown, RLD’s technology contributor, says dealers should use 2020 to get ready for increased demand for robotic mowers, autonomous mowers and connected machines. (Learn more at www.RuralLifestyleDealer.com/2020TechTrends.)

The U.S. housing market and unemployment rates are indicators as well, since the rural equipment market is driven by consumer sentiment. The year ended on a very positive note for housing, as U.S. homebuilders were the most confident they’ve been in 20 years, according to data from the National Assn. of Home Builders/Wells Fargo Housing Market Index.

And, what will the economy bring in 2020 for opportunities and challenges? Alex Chausovsky, director of speaking services with ITR Economics, says, “The economy over the course of this past year has been slowing. We’ve still had an expansion, but the expansion was happening at a decelerating pace.”

He expects a “brief and mild” low point to occur in the industrial economy (which is based in part on manufacturing) in mid-2020 and then we’ll see the next rising trend in the economy. “To be ready to take advantage of that, you need to ask yourself questions like, ‘Do I have the right people? Do I have the right capacity? What kind of equipment or CRM do I need?’” he says. Read more about ITR Economics’ forecast at www.RuralLifestyleDealer.com/2020EconomicForecast.

The national unemployment rate remains an issue for finding new talent, with December 2019 logging a rate of 3.5% compared with 4.0% for the beginning of 2019.

Lingering Concerns

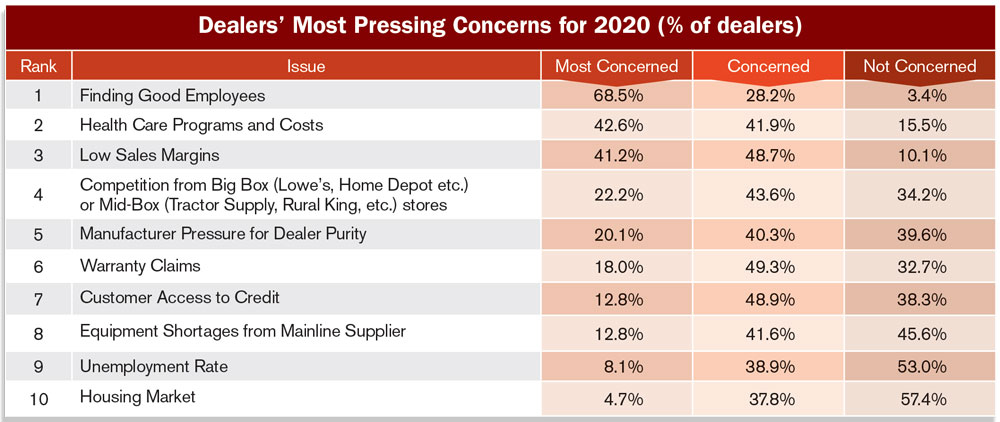

The survey also asks dealers what they are most concerned about, looking at 10 areas. Finding good employees is a problem that’s worsening. About 68% of dealers say the issue is what they are most concerned about. This is up from 61% in the 2019 survey. (See the table “Dealers’ Most Pressing Concerns” below.}

Dealers say a disconnect from agriculture, lack of work ethic and lack of interest in working at an equipment dealership are all contributing factors to the issue. “Home grown” service techs are an answer from some. Read how Eis Implement of Two Rivers, Wis., is working with a county apprenticeship program to find and train young people interested in a career in mechanics. Go to www.RuralLifestyleDealer.com/EisImplement.

Healthcare programs and costs rank second with about 42% of dealers selecting it as their “most concerned about” issue. This is up from 32% in last year’s survey. Low sales margin rank third this year, with about 42% of dealers saying this is the issue they are most concerned about. This is down slightly from 44.7% in last year’s survey.

Dealers are showing increased concern about competition from big box and mid-box stores. About 22% say this is the issue they are most concerned about vs. about 16% who expressed that sentiment last year.

Changing Industry

Consolidation continued in the industry last year. Doosan Bobcat is set to acquire the assets of BOB-CAT mowers and the Steiner and Ryan brands from Schiller Grounds Care and re-entered the compact tractor market with 15 new models.

The Alamo Group acquired Dixie Chopper and is set to acquire Morbark. Yanmar acquired ASV Holdings. Toro acquired Charles Machine Works and is set to acquire Ventrac. General Transmissions acquired Actuator Electric Motors.

Paladin Attachments and Pengo Attachments joined a division of Stanley Black & Decker. Constellation Software acquired Charter Software. And, Bad Boy announced an investment from private equity firm The Sterling Group.

Other companies marked production milestones: BigDog Mower Co. celebrated 10 years, Billy Goat 50 years and Red Wing Software 40 years. Case celebrated 50 years of skid steer manufacturing. Country Clipper celebrated 30 years of manufacturing joystick-controlled zero-turn mowers.

STIHL marked its 75th millionth unit built in America. KIOTI expanded into Canada and Kubota introduced the M8 series, its largest tractor yet with over 200 horsepower.

What’s Next?

Regardless of moderation, consolidation and other influences, the rural equipment market remains strong. An RLD poll in December showed that 75% of dealers expected to be profitable in 2019. And, dealers have a myriad of ways they are looking to grow — online sales, rental, retail improvements as well as improving service department processes and expanding outside sales.

Exclusively Online

Follow these links to read dealer comments regarding top concerns and opportunities:

www.RuralLifestyleDealer.com/2020TopConcerns

www.RuralLifestyleDealer.com/2020TopOpportunities

One dealer sums up the ongoing concerns of many others: “We’re trying to handle the volume of work at the quality and customer service levels that is our legacy — but with a limited workforce.”

Another dealer offers this outlook on opportunities: “Commercial battery products — California has a huge push to go battery and as of now there are only a few pieces in a few lines that really qualify as commercial. Landscape contractors are being pushed to go battery by their customers in a huge way.

“We’re always on the lookout for brands that promote service and quality. By far, the largest opportunity for continued growth is to continue to build our dealership’s brand and grow our dedicated customer base. No one can match our knowledge and service.”